AI반도체 계의 실리콘투?

삼지전자는 통신장비 제조와 전자유통업을 중심으로 성장 중인 코스닥 상장 기업이다. 특히 2024년 삼성전자와의 AI 반도체 유통 사업권을 따내면서 매출과 영업이익이 크게 뛴 부분이 관심이 갔다. 전자 유통업으로 24년도에 영업이익을 이렇게 올렸다고?

알고보니, 삼성전자의 AI칩 유통권을 따낸 회사 였다.

이번 분석에서는 삼지전자의 구조적 성장 가능성과 경쟁 우위, 재무 성과, 그리고 운영 효율성 측면에서의 잠재력을 살펴보며 향후 전망도 짚어보려 한다.

1. 구조적 성장 가능성이 있는 사업 영역인가?

삼지전자는 전자유통업과 통신장비 제조를 주력으로 하며, 특히 전자유통업이 매출의 약 85%를 차지하는 핵심 축이다. 이 사업은 AI 반도체, 이미지 센서(CIS), 자동차 전장 부품 같은 고부가가치 제품 유통에 집중하고 있다. 주목할 점은 삼성전자의 AI 반도체를 일본과 중국 시장에 공급하는 역할이다.

성장 가능성 포인트

- AI와 전기차 시장의 확장: 글로벌 AI 시장이 2025년에도 계속 커지고 있고, 전기차 시장도 빠르게 성장 중이다. 삼지전자는 AI 반도체(HBM, AI 칩 등) 유통으로 이 시장의 중심에 서 있다. 일본 통신사업자와 중국 전기차 제조사로의 수출이 매출을 끌어올리는 큰 동력이다.

- 5G 인프라 수요: 5G 중계기와 오픈랜 장비를 LG유플러스와 일본 시장에 공급하며 안정적인 매출을 확보하고 있다. 5G 네트워크 확산이 글로벌 트렌드인 만큼, 이 부문도 꾸준히 성장할 가능성이 높다.

- 정부 지원: 한국 정부가 반도체 산업을 전략적으로 밀어주고 있고 신정부에서의 추경이 기대된다. 삼성전자와의 협력은 이런 정책적 지원을 간접적으로 활용할 수 있는 기회를 주지 않을까.

AI와 5G라는 거대한 기술 트렌드 속에서 삼지전자는 확실히 구조적 성장을 기대할 만한 사업 영역을 가지고 있어 보인다. 특히 AI.

2. 경쟁자를 이길 만한 강점이 있나?

삼지전자의 경쟁력은 삼성전자 및 LG유플러스와의 파트너십, 일본 시장 네트워크, 그리고 고부가가치 유통 전문성에서 나온다.

강점과 해자

- 삼성전자 AI 반도체 유통권: 삼지전자는 삼성전자와의 협력으로 AI 반도체 유통권을 확보했다. 삼성전자는 TSMC, 하이닉스와 AI 반도체 시장에서 치열하게 경쟁 중인데, 현재까지 잘 못하고 있지만,, 시간문제라고 본다. 여기서 삼지전자는 일본과 아시아 시장을 공략하는 핵심 파트너로 자리잡고 삼성전자로 부터 독점 계약권을 따낸 것으로 보인다. 삼지전자의 유통력을 인정 받은 것인데 이런 관계는 쉽게 대체하기 어려운 독점적 위치라고 보고 싶다

- 일본 시장에서의 입지: 일본 통신사업자와의 협력으로 5G 장비와 반도체 유통에서 강력한 네트워크를 구축했다. 원가저감형 5G 장비 상용화와 오픈랜 제안 활동은 경쟁사와 차별화된 강점.

- LG유플러스와의 안정적 관계: LG유플러스의 5G 중계기 공급에서 60% 점유율을 차지하고 있다. 통신장비와 유통 사업 간 시너지가 안정적인 매출을 뒷받침한다.

- 고마진 제품 유통: AI 반도체와 자동차 전장 부품 같은 고부가가치 제품에 특화되어 있어 일반 유통업체와 비교해 수익성이 높다.

리스크

삼성전자와 LG유플러스에 대한 의존도가 높다는 점은 부담이다. 만약 삼성전자가 직접 유통으로 전환하거나 LG유플러스와의 계약이 줄어들면 타격이 클 수 있다. 반도체 유통 시장의 글로벌 변동성도 변수다. 그래도 현재로선 삼성전자와 일본 시장에서의 파트너십이 확실한 경쟁 우위를 제공한다.

참고로 삼성전자가 직접 유통하지 않는 이유는 공급망 효율성과 비용 절감을 위해서다. 삼성전자는 반도체 제조에 집중하고, 삼지전자의 일본 시장 네트워크와 유통 전문성을 활용해 시장 접근성을 높이고 있다.

3. 재무 성과와 현금 흐름은 기대할 만한가?

삼지전자는 2024년 실적에서 큰 성장을 보여줬다. 전자유통업과 통신장비 사업의 성과를 중심으로 살펴보자.

재무 성과

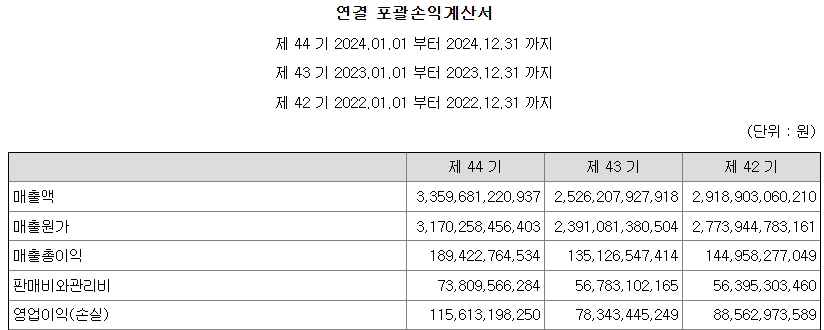

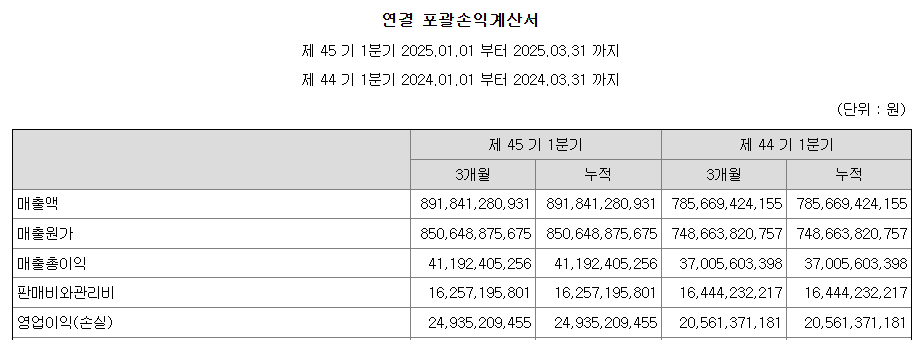

- 삼지전자는 2024년 AI 반도체 유통 사업권 획득으로 매출과 영업이익이 큰 폭으로 성장했다. 2022~2023년은 매출과 이익이 다소 정체했으나, 2024년 매출총이익과 순이익이 각각 188%, 90.9% 급증하며 재무 성과가 크게 개선. 내가 주목하게된 계기다. 2025년 1분기에는 매출과 순이익이 전년 대비 성장세를 유지했으나, 영업이익은 정체 상태. 이는 전자 부품의 1분기 출하량이 가장 저조함을 감안 했을 때 감래할 만한 수준이라 보고 싶고, 2분기의 실적 발표가 중요해 보인다.

사업별 성과

- 전자유통업: 매출의 85%를 차지하는 주력 사업이다. 2024년 삼성전자와의 AI 반도체 유통 사업권으로 급성장하며 1분기 매출 약 7,857억 원(37%↑), 영업이익 206억 원(81%↑)을 기록했다. AI 반도체와 전기차 부품 수요 증가가 주효했다.

- 통신장비 제조: LG유플러스와 일본 시장에서의 5G 장비 공급이 안정적인 매출을 만들고 있다. 매출 비중은 작지만(0.37%), 꾸준한 현금 흐름을 제공하며 유통 사업과 시너지를 낸다.

- 현금 흐름: 고마진 제품 유통으로 마진율(10~20% 추정)이 높아 영업 활동 현금 흐름이 개선되고 있다. 2024년 실적 호조로 재무 안정성이 강화되었다.

향후 전망

AI 반도체와 5G 장비 수요는 2025년에도 이어질 가능성이 높다. 삼지전자의 매출과 영업이익은 안정적으로 성장할 전망이다. 다만, 삼성전자와 LG유플러스 의존도가 높아 고객 다변화가 필요하다. 일본, 중국 외 새로운 시장(동남아시아 등)으로의 확장이 현금 흐름 안정성을 더 높일 수 있을 것이다.

4. 운영 효율성은 계속 개선되고 있나?

삼지전자는 운영 효율성을 개선하며 수익성을 높이고 있다. 2024년 실적에서도 이런 점이 잘 드러난다.

개선 사례

- 공급망 최적화: 2022~2023년 반도체 공급망 병목 현상이 풀리면서 부품 조달 비용이 안정화되었다. 이를 통해 유통 마진을 극대화했다.

- 일본 시장 원가 절감: 일본 통신사업자향 5G 장비에서 원가저감형 모델을 상용화하며 효율성을 높였다. 유통 사업과 연계된 공급망 최적화도 눈에 띈다.

- 사업 간 시너지: 통신장비와 유통 사업 간 시너지를 통해 물류 비용을 줄이고 원가를 절감했다. 5G 장비 공급에 필요한 반도체를 자체 유통망으로 조달하며 중간 비용을 낮췄다.

개선 가능성

- 고객 다변화: 삼성전자와 LG유플러스 의존도를 줄이기 위해 새로운 고객 발굴이 필요하다. 동남아시아 통신사업자나 글로벌 전기차 제조사와의 협력이 운영 리스크를 줄일 수 있다.

- 디지털화: 유통 물류 시스템의 디지털 전환으로 재고 관리와 물류 비용을 최적화할 여지가 있다. AI 기반 수요 예측 도입은 효율성을 더 높일 수 있다.

- R&D 확대: 통신장비와 2차전지 충방전 시스템에서 기술 개발을 계속하고 있다. R&D 투자가 유통 사업의 기술적 지원으로 이어지면 운영 효율성이 더 개선될 가능성이 있다.

결론: 삼지전자, AI 반도체 유통으로 주목할 만한 기업

삼지전자는 AI 반도체와 5G 장비 시장의 성장 트렌드를 타고 구조적 성장 가능성을 보여주고 있다. 특히 삼성전자와의 파트너십이 강력한 경쟁 우위를 제공하는 것으로 보이며, 급증하는 AI 반도체 수요에 삼지전자의 매출과 영업이익이 증가되기를 기대해 본다.

Samji Electronics (037460) Analysis: A KOSDAQ Company Poised for Growth Through AI Chip Distribution

June 4, 2025 | By Growth-Papa

Could this be the Silicon Two of the AI chip world?

Samji Electronics is a KOSDAQ-listed company growing through its focus on telecommunications equipment manufacturing and electronic distribution. What caught my eye was how the company significantly boosted its sales and operating profit in 2024 after securing the AI chip distribution rights from Samsung Electronics. How did they manage to increase their operating profit so much in 2024 through electronic distribution?

Turns out, Samji Electronics is the company that won the distribution rights for Samsung Electronics’ AI chips.

In this analysis, I’ll dive into Samji Electronics’ potential for structural growth, competitive strengths, financial performance, and operational efficiency, while also touching on its future outlook.

1. Does It Have a Business Area with Structural Growth Potential?

Samji Electronics focuses on electronic distribution and telecommunications equipment manufacturing, with electronic distribution accounting for about 85% of its revenue, making it the company’s core pillar. This business centers on distributing high-value products like AI chips, image sensors (CIS), and automotive electronic components. A key highlight is its role in supplying Samsung Electronics’ AI chips to markets in Japan and China.

Growth Potential Highlights

- Expansion of AI and EV Markets: The global AI market continues to grow in 2025, and the electric vehicle (EV) market is also expanding rapidly. Samji Electronics is right at the heart of this trend with its AI chip distribution (HBM, AI chips, etc.). Exports to Japanese telecom companies and Chinese EV manufacturers are a major driver of revenue growth.

- Demand for 5G Infrastructure: Samji supplies 5G repeaters and Open RAN equipment to LG Uplus and the Japanese market, securing stable revenue. With 5G network expansion being a global trend, this segment has solid growth potential.

- Government Support: The South Korean government is strategically supporting the semiconductor industry, and there’s anticipation for supplementary budgets under the new administration. Collaboration with Samsung Electronics likely gives Samji an indirect opportunity to benefit from such policy support.

In the midst of massive tech trends like AI and 5G, Samji Electronics seems to have a business area with clear structural growth potential—especially in AI.

2. Does It Have a Competitive Edge to Beat Rivals?

Samji Electronics’ competitive strengths stem from its partnerships with Samsung Electronics and LG Uplus, its network in the Japanese market, and its expertise in high-margin distribution.

Strengths and Moats

- Samsung Electronics AI Chip Distribution Rights: Samji secured AI chip distribution rights through its collaboration with Samsung Electronics. Samsung is fiercely competing with TSMC and SK Hynix in the AI chip market, and while it hasn’t dominated yet, I believe it’s only a matter of time. Here, Samji has positioned itself as a key partner for targeting Japan and other Asian markets, seemingly securing an exclusive distribution contract from Samsung. This recognition of Samji’s distribution capabilities creates a monopolistic position that’s hard to replace.

- Foothold in the Japanese Market: Through partnerships with Japanese telecom companies, Samji has built a strong network for 5G equipment and chip distribution. Its cost-efficient 5G equipment commercialization and Open RAN proposals set it apart from competitors.

- Stable Relationship with LG Uplus: Samji holds a 60% share in supplying 5G repeaters to LG Uplus. The synergy between its telecom equipment and distribution businesses supports stable revenue.

- High-Margin Product Distribution: Specializing in high-value products like AI chips and automotive components gives Samji better profitability compared to typical distributors.

Risks

The high reliance on Samsung Electronics and LG Uplus is a concern. If Samsung shifts to direct distribution or if LG Uplus reduces its contracts, the impact could be significant. Global volatility in the chip distribution market is another variable. Still, for now, Samji’s partnership with Samsung and its foothold in Japan provide a solid competitive edge.

For reference, the reason Samsung doesn’t handle distribution directly is to optimize supply chain efficiency and cut costs. Samsung focuses on chip manufacturing while leveraging Samji’s Japanese market network and distribution expertise to enhance market access.

3. Is Its Financial Performance and Cash Flow Promising?

Samji Electronics showed impressive growth in its 2024 financials. Let’s break down the performance of its electronic distribution and telecom equipment businesses.

Financial Performance

Samji achieved significant growth in revenue and operating profit in 2024, driven by its AI chip distribution rights from Samsung. Between 2022 and 2023, revenue and profits were somewhat stagnant, but in 2024, gross profit and net profit surged by 188% and 90.9%, respectively, marking a major improvement in financial performance. That’s what caught my attention. In Q1 2025, revenue and net profit maintained their growth trend compared to the previous year, but operating profit remained flat. Considering that Q1 typically sees the lowest shipment volumes for electronic components, this seems acceptable, and the Q2 earnings announcement will be crucial to watch.

Segment Performance

- Electronic Distribution: This segment accounts for 85% of revenue and is the company’s main driver. In 2024, it grew rapidly thanks to the AI chip distribution deal with Samsung, recording Q1 revenue of approximately 785.7 billion KRW (up 37%) and an operating profit of 20.6 billion KRW (up 81%). Rising demand for AI chips and EV components played a key role.

- Telecom Equipment Manufacturing: Supplying 5G equipment to LG Uplus and the Japanese market generates stable revenue. While its revenue share is small (0.37%), it provides consistent cash flow and synergies with the distribution business.

- Cash Flow: High-margin product distribution, with estimated margins of 10-20%, has improved operating cash flow. The strong 2024 performance has also bolstered financial stability.

Future Outlook

Demand for AI chips and 5G equipment is likely to continue into 2025, and Samji’s revenue and operating profit are expected to grow steadily. However, its heavy reliance on Samsung and LG Uplus calls for customer diversification. Expanding into new markets beyond Japan and China, such as Southeast Asia, could further stabilize cash flow.

4. Is Operational Efficiency Continuously Improving?

Samji Electronics is enhancing its profitability through operational efficiency improvements, which are evident in its 2024 performance.

Improvement Examples

- Supply Chain Optimization: The resolution of semiconductor supply chain bottlenecks in 2022-2023 stabilized component procurement costs, allowing Samji to maximize distribution margins.

- Cost Reduction in Japan: Samji improved efficiency by commercializing cost-efficient 5G equipment models for Japanese telecom companies. Supply chain optimization tied to its distribution business also stands out.

- Synergies Between Segments: By leveraging synergies between its telecom equipment and distribution businesses, Samji reduced logistics costs and overall expenses. For instance, it sources chips for 5G equipment through its own distribution network, cutting intermediary costs.

Areas for Improvement

- Customer Diversification: Reducing reliance on Samsung and LG Uplus by finding new customers is essential. Partnerships with Southeast Asian telecom companies or global EV manufacturers could lower operational risks.

- Digitalization: Digitizing the distribution and logistics systems could optimize inventory management and reduce costs. Introducing AI-based demand forecasting could further boost efficiency.

- R&D Expansion: Samji continues to invest in R&D for telecom equipment and battery charging/discharging systems. If these investments translate into technical support for its distribution business, operational efficiency could improve further.

Conclusion: Samji Electronics, a Noteworthy Player in AI Chip Distribution

Samji Electronics is riding the growth trends of AI chips and 5G equipment, showing strong potential for structural growth. Its partnership with Samsung, in particular, provides a robust competitive advantage, and I’m looking forward to seeing how the rising demand for AI chips will drive Samji’s revenue and operating profit higher. While there are risks like its reliance on key partners, the company’s operational efficiency improvements and financial stability make it a compelling player to watch. If the AI and 5G markets continue to expand in 2025, Samji Electronics could be poised for even greater growth.

This analysis covers Samji Electronics’ business and financial performance, but further market research and risk assessment are necessary before making investment decisions. Curious about Samji’s future? Let’s keep an eye on it!