거시적인 글로벌 현황

2025년 3월, 글로벌 경제는 변화의 갈림길에 서 있다. 러시아-우크라이나 전쟁은 점차 해결될 기미를 보이며 지정학적 긴장이 완화될 조짐을 드러내고 있고, 이는 유럽에 새로운 희망을 주고 있어 보인다. 반면, 미국의 ‘자국 우선주의’ 아래 트럼프 행정부가 유럽에 안보와 경제적 자립을 요구하며 압박을 지속하고 있고, 중국의 성장 둔화와 원자재 가격 변동은 여전히 공급망에 영향을 미치고 있다. 이런 복잡한 환경 속에서 유럽은 재정 확대를 통해 경제 회복과 에너지 안보를 강화하려는 움직임을 보이고 있으며, 이는 투자자들에게 매력적인 기회를 열어주고 있다.

유로존의 현재 상황

유로존은 최근 인플레이션 둔화(2025년 2월 CPI 2.3%, 예비치 2.4%에서 하향)로 ECB의 금리 인하 기대감을 키우며 숨통을 틔우고 있다. 하지만 독일 경제는 2023년 -0.3%, 2024년 -0.1%(독일 연방통계청 추정)로 두 해 연속 역성장을 겪으며 회복이 시급한 상황. 이런 가운데 독일이 헌법을 개정하며 약 1조 유로(정확히 1조 유로, 약 1580조 원) 규모의 재정 지출을 결정한 건 큰 전환점으로 보인다:

- 인프라 투자: 5000억 유로(약 790조 원, 독일 연방의회 자료)로 교통, 에너지, 디지털 인프라를 업그레이드.

- 국방비 확대: GDP 3.5% 수준(연간 약 1400~1500억 유로, 킬세계경제연구소 분석)으로 부채 한도를 해제하고 재무장에 나섬.

- 기후 예산: 5000억 유로 중 1000억 유로(약 158조 원)를 기후 변화 대응에 배정.

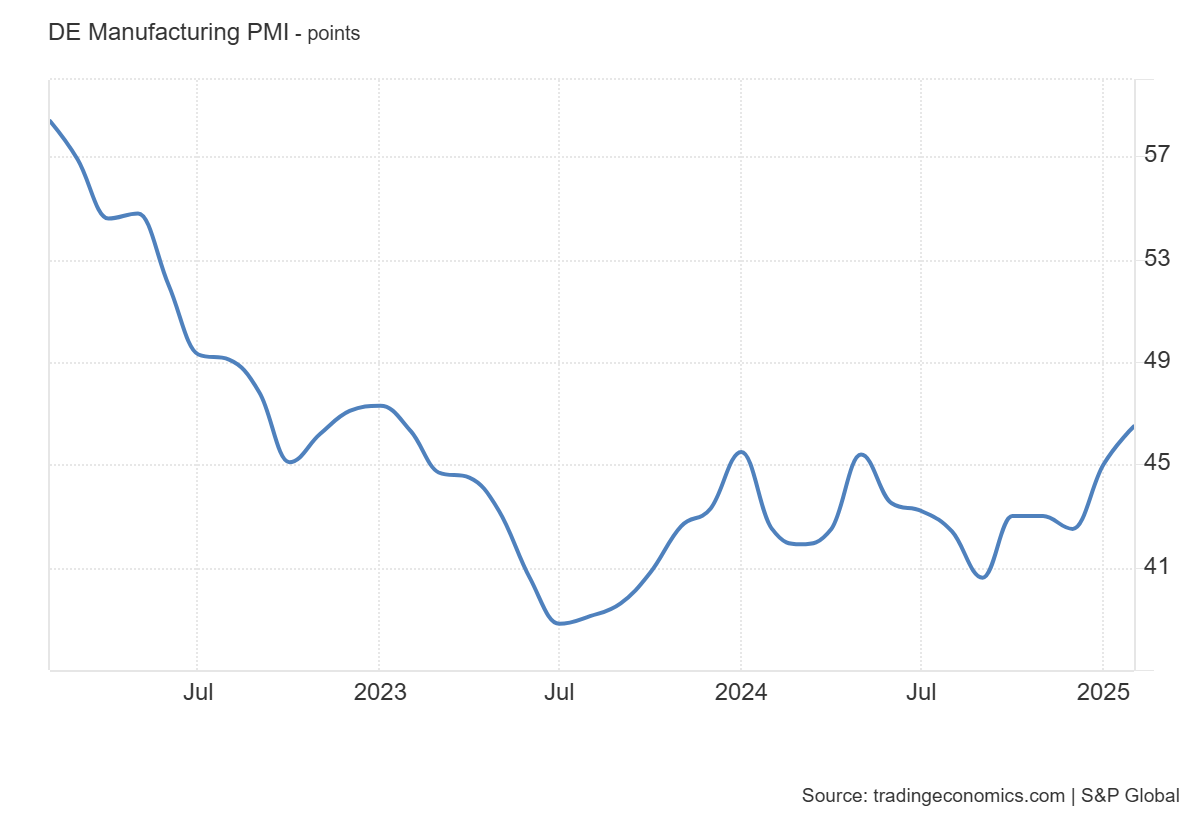

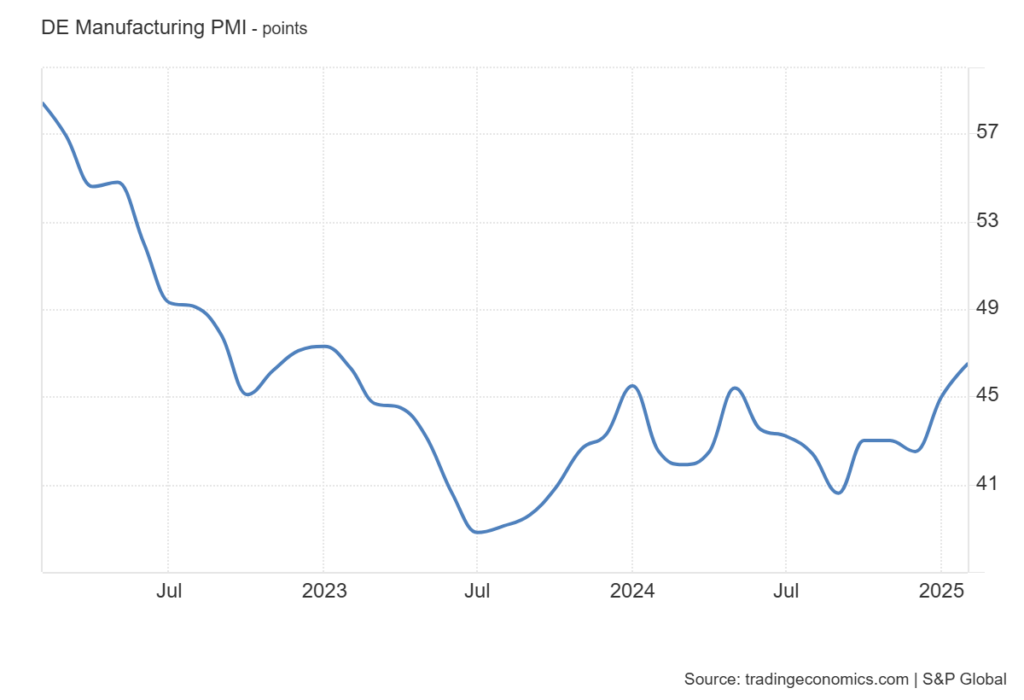

이 재정 확대는 독일 경제를 되살리고 유로존 전체에 활력을 불어넣을 가능성이 높다. 독일경제연구소(DIW)는 2026년 성장률 전망치를 1.1%에서 2.1%로 상향 조정했고, DAX 40 지수는 2025년 3월 기준 사상 최고치를 경신, 독일의 PMI도 반등 기조가 눈에 띈다. 이제 이 흐름을 활용할 기업을 찾는 게 핵심.

지멘스가 눈에 띄는 이유

지멘스(Siemens, SIE.DE)는 이 변화의 중심에 서 있는 기업이다. 독일 뮌헨과 베를린에 본사를 둔 이 글로벌 기술 대기업은 산업 자동화, 스마트 인프라, 모빌리티 분야에서 선두를 달리고 있다. 지멘스가 주목받는 이유는 아래로 살펴 봄 :

- 인프라와의 직접 연계: 독일의 5000억 유로 인프라 예산은 지멘스의 스마트 인프라(전력망, 데이터 센터)와 모빌리티(철도, 수소 열차)에 직접 투입될 가능성이 높다. 2024 회계연도(2023.10~2024.9) 스마트 인프라 이익은 37억 유로(지멘스 연례보고서, 마진 17.3%), 모빌리티 매출은 109억 유로로 이미 강세를 기록.

- 제조업 회복의 핵심: 디지털 인더스트리 부문은 공장 자동화와 소프트웨어로 독일 제조업(수출의 약 31%, 독일 연방통계청)을 부흥시킬 기술을 제공한다. 2024년 매출 198억 유로로 약간 주춤했지만(-1.2%), 재정 확대가 제조업에 숨을 불어넣으면 반등할 준비가 돼 있다고 봤다.

- 안정성과 성장성: 2024년 순이익 89억 유로(전년 84억 유로 대비 5.95% 증가), Free Cash Flow 95억 유로(지멘스 공식 발표)로 안정적인 기반 위에 성장 잠재력을 갖췄다.

지멘스는 독일 경제가 재가동되는 순간, 그 심장부에서 뛰며 실적을 끌어올릴 가능성이 크다고 봤다.

함께 볼 만한 다른 기업

지멘스 외에도 유로존의 재정 확대와 경제 회복에서 주목할 만한 기업:

- Rheinmetall (RHM.DE): 방산 기업으로, 국방비 확대의 최대 수혜자. 2024년 매출 79억 유로(24% 증가), 2025년 100억 유로 예상(회사 전망).

- VINCI (DG.PA): 프랑스 건설·인프라 대기업. 도로, 공항, 에너지망에서 강하며, 전쟁 해결 후 재건 시나리오에서 유망(2024년 순이익 49억 유로, VINCI 실적 발표).

- Nordex (NDX1.DE): 풍력 전문 소형주로, 기후 예산에서 중장기 성장 가능성(2024년 매출 65억 유로, 흑자 전환 기대).

Rheinmetall은 방산 모멘텀이 강력하고, VINCI는 장기 안정성, Nordex는 소규모 성장성이 돋보인다.

그래도 지멘스가 매력적인 이유

지멘스가 여전히 매력적인 이유는 세 가지:

- 즉각적인 수혜: 독일의 인프라·제조 투자가 2025년부터 본격화되면, 지멘스의 수주 잔고(2024년 1133억 유로, 지멘스 자료)가 빠르게 매출과 이익으로 전환될 수 있어 보인다.

- 공격적 성장 가능성: 현재 전망(2025년 매출 성장률 4~7%, 이익 성장률 5~10%)보다 재정 확대가 뒷받침되면 매출 8~12%, 이익 10~15%까지 뛸 잠재력이 있다고 봤다.

- 리스크 분산: 다각화된 사업 구조로 단일 테마에 의존하지 않고, 인프라와 제조 전반을 아우르며 안정성을 확보.

지멘스는 유럽 경제가 회복하는 과정에서 단기 성과와 중기 성장성을 동시에 잡을 수 있는 균형 잡힌 선택으로 보였다.

결론

유로존은 지금 역사적인 재정 확대를 통해 경제를 살리려는 중대한 전환점. 독일의 인프라와 제조 투자는 경제 회복의 핵심 동력으로 작용하며, 그 중심에 지멘스가 서 있다. 안정적인 이익 기반 위에서 공격적인 성장을 기대할 수 있는 지멘스는, 2025년 상반기 정책 집행과 함께 실적 반등을 노릴 수 있는 기회의 문으로 보인다.

돈은 부끄러움이 많아 사람들의 시선을 피한다. 사람들의 시선이 몰린 곳으로부터 다시 기회가 될 곳을 찾아가 보자.

Europe’s Economic Revival and Siemens: Why It’s Worth Watching Now

The Big Global Picture

As of March 2025, the global economy’s standing at a crossroads. The Russia-Ukraine war is starting to show signs of winding down, easing geopolitical tensions and giving Europe a glimmer of hope. Meanwhile, Trump’s “America First” stance keeps pushing Europe to stand on its own in terms of security and economic independence. China’s slowing growth and volatile raw material prices are still rattling supply chains. In this messy mix, Europe’s stepping up with massive fiscal expansion to boost its economy and energy security—opening up some pretty sweet opportunities for investors.

What’s Happening in the Eurozone

The Eurozone’s catching a break with inflation cooling off—February 2025 CPI hit 2.3%, down from a preliminary 2.4%, stoking hopes for ECB rate cuts. But Germany’s economy isn’t out of the woods yet, posting -0.3% growth in 2023 and -0.1% in 2024 (German Federal Statistical Office estimates), marking two straight years of contraction. Things need a turnaround, fast. Enter Germany’s game-changer: a constitutional amendment unlocking about 1 trillion euros (exactly 1T euros, roughly 1.58T USD) in fiscal spending:

- Infrastructure Investment: 500B euros (~790T USD, per German Bundestag data) to upgrade transport, energy, and digital infrastructure.

- Defense Boost: Targeting 3.5% of GDP (~140B–150B euros annually, Kiel Institute analysis), scrapping debt limits for rearmament.

- Climate Budget: 100B euros (~158T USD) of that 500B earmarked for climate action.

This cash injection’s got a real shot at reviving Germany’s economy and breathing life into the broader Eurozone. The German Economic Institute (DIW) bumped its 2026 growth forecast from 1.1% to 2.1%, and the DAX 40 index is hitting all-time highs as of March 2025, signaling market optimism. The trick now is finding the companies that’ll ride this wave.

Why Siemens Stands Out

Siemens (SIE.DE) is right at the heart of this shift. Based in Munich and Berlin, this global tech giant’s a leader in industrial automation, smart infrastructure, and mobility. Here’s why I’ve got my eye on it:

- Tied to Infrastructure: Germany’s 500B-euro infra budget lines up perfectly with Siemens’ smart infrastructure (power grids, data centers) and mobility (rail, hydrogen trains). In its 2024 fiscal year (Oct 2023–Sep 2024), smart infra raked in 3.7B euros in profit (17.3% margin, Siemens annual report), while mobility pulled in 10.9B euros in revenue—already showing strength.

- Key to Manufacturing Revival: The Digital Industries arm, with factory automation and software, is set to boost Germany’s manufacturing sector (about 31% of exports, per Federal Statistical Office). It dipped to 19.8B euros in 2024 revenue (-1.2%), but I see it bouncing back once fiscal spending kicks in.

- Stability Meets Growth: 2024 net income hit 8.9B euros (up 5.95% from 8.4B the prior year), with free cash flow at 9.5B euros (Siemens official data). It’s got a solid base and room to grow.

I figure Siemens is poised to jump when Germany’s economy fires up again, driving results from the core.

Other Companies Worth a Look

Beyond Siemens, here are some Eurozone players catching attention in this fiscal boom:

- Rheinmetall (RHM.DE): Defense champ cashing in on the military budget spike—2024 revenue at 7.9B euros (up 24%), eyeing 10B in 2025 (company outlook).

- VINCI (DG.PA): French construction and infra giant, strong in roads, airports, and energy grids, primed for post-war rebuilding (2024 net income 4.9B euros, VINCI earnings).

- Nordex (NDX1.DE): Small wind power player with mid-to-long-term upside from the climate budget (2024 revenue 6.5B euros, expecting breakeven).

Rheinmetall’s got defense momentum, VINCI offers long-term stability, and Nordex brings small-cap growth potential.

Why Siemens Still Shines

Here’s why Siemens keeps pulling me in:

- Immediate Impact: Once Germany’s infra and manufacturing investments kick off in 2025, Siemens’ order backlog (11.33B euros in 2024, Siemens data) could turn into revenue and profit fast.

- Aggressive Growth Potential: Current forecasts (2025 revenue growth 4–7%, profit growth 5–10%) could jump to 8–12% revenue and 10–15% profit with fiscal backing. Smart infra and mobility margins (17.3% and 8.8%) make it plausible.

- Risk Spread: Its diversified setup—spanning infra and manufacturing—keeps it steady without betting on just one theme.

Siemens feels like a balanced pick, nailing short-term wins and mid-term growth in Europe’s recovery.

Wrapping It Up

The Eurozone’s at a pivotal moment, pumping historic cash to revive its economy. Germany’s infra and manufacturing push is the beating heart of this turnaround, and Siemens is right there in the thick of it. With a stable profit base and the potential for aggressive growth, it’s a door to opportunity as policy execution ramps up in early 2025. Money’s shy—it ducks the spotlight. Let’s dodge the crowd and hunt where the next chance lies.