The AI power war has begun, and Solar+ESS is emerging as the ultimate solution. Electricity is now more precious than GPUs. A single AI data center consumes as much power as an entire nuclear reactor. Yet when that electricity gets funneled into data centers, there isn’t enough left for ordinary industry and households. AI infrastructure and the existing economy are on a direct collision course over the same grid. This is the fundamental problem facing the US power market right now.

I have been tracking Solar+ESS as the defining power theme of 2026 since January. “Solar? Isn’t that old news — killed off by Chinese oversupply?” Many still ask. In 2025, that view was correct. It was a period of oversupply, price collapse, and brutal attrition. 2026 is different. I believe we are at the very beginning of an upcycle — the survivors’ feast is starting. Here is the case, in numbers and facts.

① When AI Monopolizes Power, Everyone Else Goes Hungry — The Problem of Firm Power Allocation

The power shortage is real. But the crux of the problem isn’t simply a supply deficit; it’s structural asymmetry. Data centers require Firm Power: electricity that cannot be interrupted for even a second. In the near term, SOFC (solid oxide fuel cells) fill that role; medium term, gas turbines; long term, SMRs (small modular reactors). Solar+ESS cannot serve as the primary power source for data centers.

Yet the very reason Solar+ESS becomes indispensable lies in this limitation. The more Firm Power gets redirected to AI data centers, the more expensive and scarce electricity becomes for ordinary households and industry. Solar+ESS is the only tool that resolves this asymmetry — generating power through solar during the day, storing it in ESS, and discharging during the evening peak to stabilize the grid. Without this grid balancing mechanism, expanding AI infrastructure simply accelerates the transfer of electricity away from the broader economy. This is why the Trump administration — after turning its back on renewables — has started to embrace them again.

② The 99% Even Trump Can’t Stop — What the EIA Data Shows

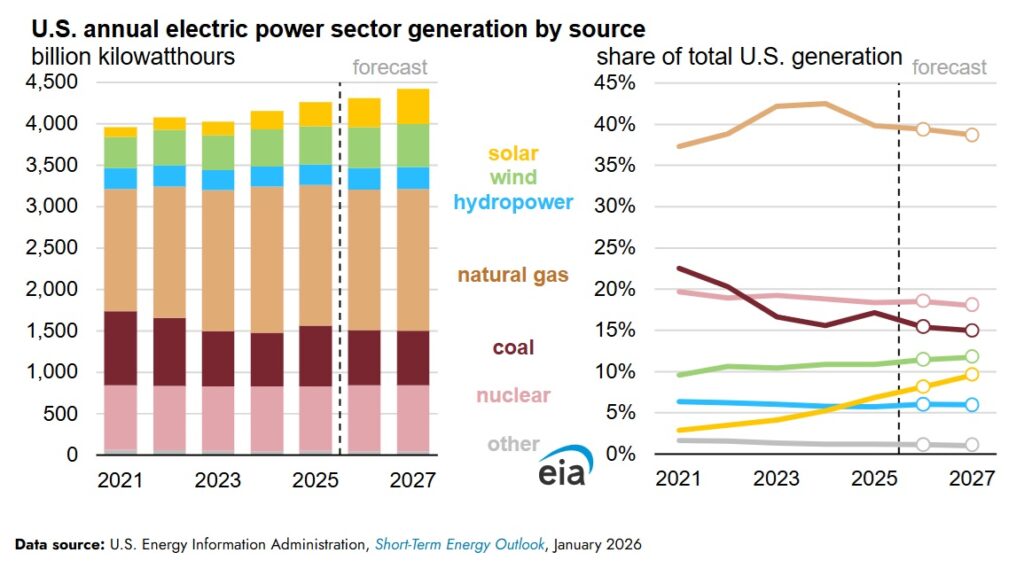

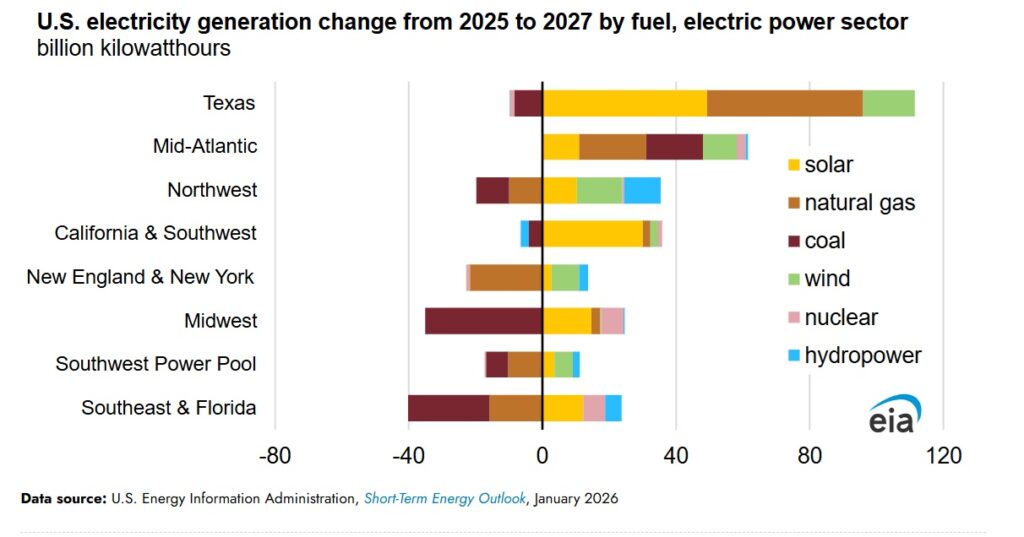

The Trump administration prioritizes fossil fuels. Yet EIA (US Energy Information Administration) data points in exactly the opposite direction. Over 99% of net new US power capacity additions in 2026 are projected to come from solar, wind, and battery storage (BESS). Renewables+BESS new capacity: 75.6GW. Fossil fuels: 4GW of gas additions, offset by 3.4GW of retirements — effectively flat. Utility solar +67%, BESS +61%, wind +154%.

This isn’t a political choice. It’s because Solar+ESS is the fastest and most practical tool available for meeting AI data center power demand while stabilizing the broader grid. DOGE adviser Katie Miller stated that “solar is more important to America than coal,” and Trump himself shared solar content on Truth Social. Mirae Asset Securities characterized this as “the early realization of an All-of-the-Above energy policy.” The signal is clear: solar has moved beyond political risk.

③ Big Tech Has Already Bought the Fields

Watch what they do, not what they say. Alphabet made its move by acquiring Solar+ESS developer Intersect Power for $4.75 billion in December 2025 — one of the largest energy infrastructure deals in history. Panels from First Solar, storage from Tesla Megapack. A declaration that data center expansion and power development will now be directly linked. Google signed a 30MW solar PPA in Malaysia — a signal that solar PPA is becoming the default power procurement option for data centers not just in the US and Europe, but across Southeast Asia as well. Tesla is building 500MWac of solar paired with 2GWh of Megapack ESS in Kern County, California — one of the largest Solar+Storage projects in the United States, capable of powering 467,000 homes annually.

Elon Musk has long argued that the fastest way to expand US energy production isn’t to build new power plants — it’s to flatten the output curve of existing ones using Megapack. The system is already moving in that direction.

④ China’s Restructuring + Non-Chinese Supply Chains Locked In — The Supply Side Is Changing Too

It’s not just demand that’s exploding. Supply structure is being simultaneously reorganized. China’s government has abolished VAT export rebates on 249 product categories, including solar cells, and issued warnings against irresponsible, predatory pricing competition. Jinko Solar has announced module price increases of up to 50% starting in March — a signal that the floor of the oversupply attrition game has been reached.

In the US, guidance for the IRA’s Domestic Content / FEOC provisions has been officially confirmed for the first time. Starting with projects breaking ground in 2026, solar must use at least 40% non-Chinese components and ESS at least 55% to qualify for tax credits. These thresholds are set to rise annually, culminating in 65% for solar and 75% for ESS by 2030. A structurally advantaged environment for companies with non-Chinese supply chains is now written into law. First Solar took an earnings hit from tariff issues at its Malaysia and Vietnam facilities — but paradoxically, the data proved that US-made modules command a 27% price premium over the global average. Having a factory inside the United States has become a genuine moat.

⑤ The Value Chain Map — Who’s in This Fight

The Solar+ESS supply chain has six distinct layers.

Polysilicon — The Scarcity of Non-Chinese Supply Non-Chinese polysilicon capacity represents just 2% of global supply. No new capacity additions are planned through 2028. Global players include REC Silicon (RECSI), Tongwei (600438), and GCL Technology (3800). In Korea, OCI Holdings (010060) is effectively the only company capable of supplying non-Chinese polysilicon at meaningful scale.

Cells & Modules — The Moat of US Domestic Production First Solar (FSLR) is the only major player with zero dependence on Chinese supply chains, collecting IRA tax credits directly from its Ohio, Alabama, and Louisiana facilities. In China, Jinko Solar (688223), Trina Solar (688599), and JA Solar (002459) are consolidating survivor positions post-restructuring. In Korea, Hanwha Solutions (009830) is the only company with a US factory (Georgia), and HD Hyundai Energy Solutions (267250) has achieved 28.7% efficiency in dry-deposition tandem cells — a world-leading result for that specific process.

Inverters & BOS — The Gateway to the Grid Enphase (ENPH) and SolarEdge (SEDG) dominate the US market. In China, Sungrow (300274) simultaneously holds the global #1 position in both ESS systems and inverters. In Korea, LS Electric (010120) leads the DC distribution market.

Trackers & Mounting — Squeezing Efficiency from Limited Land NextTracker (NXT) holds a commanding #1 position — structured to absorb installation volume growth directly as solar CAPEX expands.

ESS Systems — The Age of Storage Tesla’s Megapack and Fluence Energy (FLNC) split the market between them. Battery cells are abundant; system integrators capable of deploying them are not. In China, Sungrow, CATL (300750), and BYD (002594) compete for position. Korean beneficiaries riding this wave include Sojin System (178320, ESS enclosures), Sanil Electric (062040, ESS specialty transformers), Hanjung ENS (107640, liquid-cooled ESS thermal management), Samsung SDI, and LG Energy Solution.

Grid Infrastructure — The Circulatory System of Scale GE Vernova (GEV) and Eaton (ETN) are the backbone of US grid infrastructure. Korean equivalents include Doosan Enerbility, HD Hyundai Electric, LS Electric, and Hyosung Heavy Industries. Sanil Electric is GE Vernova’s directly chosen partner for ESS specialty transformers.

Investor Perspective: Two Questions That Matter

Two questions define this value chain. First: which companies occupy irreplaceable positions in the supply chain? Non-Chinese polysilicon, US domestic module production, ESS specialty transformers, liquid cooling — companies holding these positions gain pricing power as demand expands. Second: which companies will see their earnings estimates revised upward? When Section 232 confirmation, polysilicon price normalization, and BESS installation growth materialize, some companies’ EPS estimates will look nothing like they do today. The more useful question in this cycle isn’t how far a stock is from its current target price — it’s which companies will see their target prices raised.

The signals that would break this thesis are equally clear: a meaningful slowdown in US AI infrastructure investment, a significant rollback of IRA tax credit provisions, or a faster-than-expected completion of China’s restructuring that reignites oversupply.

Closing

A few months from now, when people start saying “I hear Solar+ESS is the only answer in this power-driven market — are there any remaining laggards that haven’t run yet?” — the judgment of someone who understood this structure early will be fundamentally different from someone who didn’t.

I have been tracking relevant companies’ news, developments, and valuations directly every month since January. This piece covered direction and structure only. For deeper analysis, please visit the deep research in the profile link.

Good fields are entered quietly. Which companies are worth planting seeds in — and the numbers behind that conviction — are all there waiting.

Disclaimer: This article is for informational purposes only and does not constitute a recommendation to buy or sell any specific security. All investment decisions and their outcomes remain the sole responsibility of the investor.