In 2026, the tech world faces a critical challenge: the AI power bottleneck.

The true constraint in the AI era isn’t GPUs—it’s electricity. Here’s a comprehensive timeline breakdown of the “power war” where Big Tech is pouring trillions into securing energy infrastructure to solve this AI power bottleneck (This post distills the essential framework from my premium research report, focusing on the core narrative you need to understand the entire flow.)

Introduction: Big Tech Secures Power with Gas, While the US Grid Stabilizes with Solar + ESS

The pace of AI technological advancement in the United States is moving at the speed of light. However, the electrical grid infrastructure needed to support it is frustratingly slow for both government officials and Big Tech executives.

Right now, Silicon Valley’s tech giants are more focused on securing electricity than acquiring NVIDIA GPUs.

AI data centers require hundreds of megawatts of power running 24/7. However, regional transmission networks and power plant expansion simply cannot keep pace with this demand. As a result, Big Tech and AI labs are pivoting sharply toward a “Build Your Own Grid (BYOG)” approach rather than waiting for the sluggish public grid.

Below, I break down the ripple effects created by this massive bottleneck and trace where capital will inevitably flow—across short-term, medium-term, and long-term horizons.

1. Immediate Term (Now ~ 1-2 Years): “Speed Over Cost”

Keyword: Speed is Moat

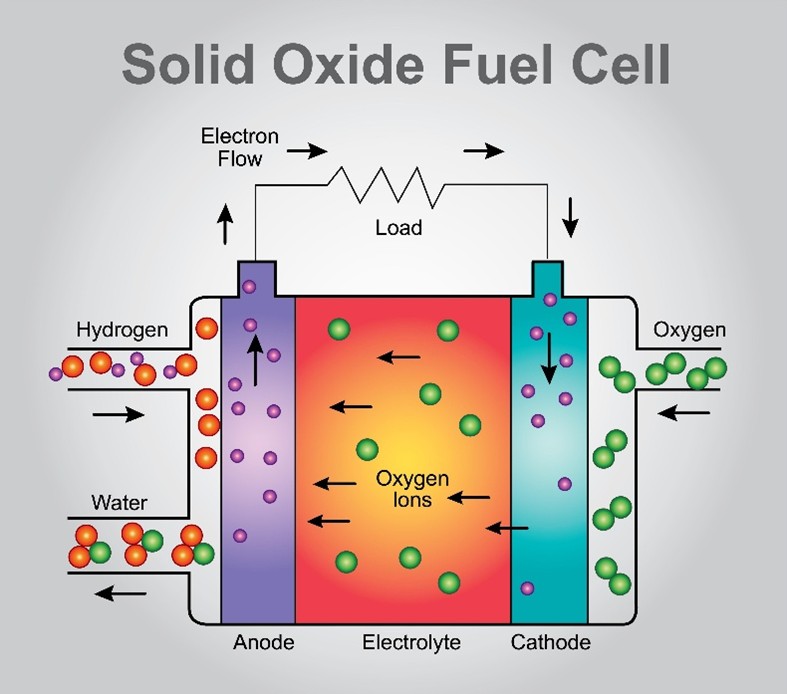

For Big Tech, every day of delay means hundreds of millions in losses. They cannot wait 5 years for grid connections, so they are seeking “plug-and-play” solutions even if they cost more. The answer: SOFC (Solid Oxide Fuel Cells).

Solution: Bloom Energy (BE)

SOFC systems deliver efficiency approaching combined-cycle gas plants while being easier to permit. They are modular—just lay them down, and you can supply tens to hundreds of megawatts within weeks or months. While CapEx is expensive ($3,000–4,000 per kW), they serve as the “relief pitcher” for urgent AI campus power needs.

Bloom Energy leads this sector. However, they have acknowledged their own production bottlenecks, raising questions about whether the strong 2025 narrative can fully carry into 2026.

2. Medium Term (2-5 Years): “The Gas Turbine War and the Rise of Reciprocating Engines”

Keyword: Gas Turbine Shortage & Hybrid Solutions

Once immediate responses are deployed, the only reliable source for large-scale, stable power is Natural Gas. Here is where the problems emerge:

Gas Turbine Supply Crunch: The global “Big Three” (GE Vernova, Siemens Energy, Mitsubishi Power) have years of backlog for large H-Class turbines, with lead times stretching to 2–4 years. It is literally a “name your price” situation.

New Player Spotlight: Doosan Enerbility Emerging from this gap is South Korea’s Doosan Enerbility. Armed with their self-developed H-class turbine (DGT6), they secured Elon Musk’s xAI project (approx. 1.9GW), making a spectacular entrance as a “new major player in the global gas turbine market.” As they capture the spillover that established players cannot handle, their growth story is just beginning.

Plan B: Reciprocating Engine (RICE) Fleets With turbine shortages, companies are deploying hundreds of reciprocating engines—originally designed for ships and aircraft—clustered together. Wärtsilä, Jenbacher, MTU, and Rolls-Royce are bundling dozens to hundreds of 3–20MW engines to create GW-scale on-site power plants. The lengths they are going to solve turbine shortages is remarkable—it is almost wartime-level mobilization, reflecting just how urgent the energy shortage has become.

3. Long Term (5-10+ Years): The Path Leads to SMR (feat. Nuclear Foundries)

On-site gas is fundamentally fossil fuel-based, making it vulnerable to long-term carbon regulations, fuel costs, and political risks. This is where SMR (Small Modular Reactors) emerge as “the ultimate solution for 5–10 years out.”

SMR Ecosystem: Designers vs. Manufacturers Think of the SMR ecosystem like semiconductors: Fabless (Design) vs. Foundry (Manufacturing).

① Design & Operations (Fabless)

- CCJ (Cameco): Holds a stake in Westinghouse, essentially serving as a Westinghouse proxy investment.

- Oklo (OKLO): Announced multi-GW LOIs/frameworks with Meta, Constellation, etc. (early-stage option contracts).

- NuScale (SMR): Has NRC design certification but is facing commercialization challenges after the UAMPS project cancellation.

- GE Hitachi: Showing the fastest commercialization progress with the BWRX-300 at Canada’s Darlington site.

② Manufacturing & Supply Chain (Foundry)

- BWX Technologies (BWXT): “The TSMC of Nuclear.” One of North America’s most critical N-stamp nuclear equipment manufacturers. Secured $700M+ contracts for GE Hitachi’s BWRX-300, with guaranteed stable cash flow from exclusive US Navy reactor supply.

③ Fuel & Platforms

- Uranium: From mining to raw materials—Cameco (CCJ); enrichment key player—Centrus Energy (LEU).

Key Insight: Whether Oklo, NuScale, or GEH wins, BWXT benefits as the “common subcontractor to multiple SMR winners.” Think of BWXT as the US equivalent of Korea’s Doosan Enerbility.

4. Grid Relief: Solar + ESS

But for all these power sources to work properly, grid-wide stabilization is essential. The most realistic structure: Data centers rely on ‘Firm Power’ from gas and nuclear, while general electricity demand gets supported by ‘Solar + ESS’ to shave peaks.

- Solar: First Solar (FSLR), Nextracker (NXT), HD Hyundai Energy Solutions

- ESS: Fluence Energy (FLNC), Sanil Electric, Seojin System

Solar + ESS plays a critical role across the grid—supporting general demand and shaving peaks so remaining Firm Power can serve data centers. While they may not be Big Tech’s direct large-scale power source, they are the most powerful realistic alternative for general industrial and residential electricity shortages. This sector requires national policy support.

Particularly as policy-driven restructuring begins for Chinese solar companies, 2026 is likely the year solar sector narratives revive. (Note: Sanil Electric and Seojin System are core companies that can move in lockstep with global ESS value chain leaders.)

5. Core Infrastructure Spanning All Generation Types

Are there players that transcend specific generation types and span the entire spectrum? This question brings up VST, SNT Energy, and ETN.

① Vistra Corp (VST): The Ultimate All-Rounder An integrated power company with large-scale gas plants + existing nuclear + renewables/ESS, capable of handling short-term (gas) → medium-term (nuclear PPA) → long-term (SMR). It is a “Gas + Nuclear + SMR” triple-threat platform. (NextEra Energy (NEE) is pursuing a similar portfolio.)

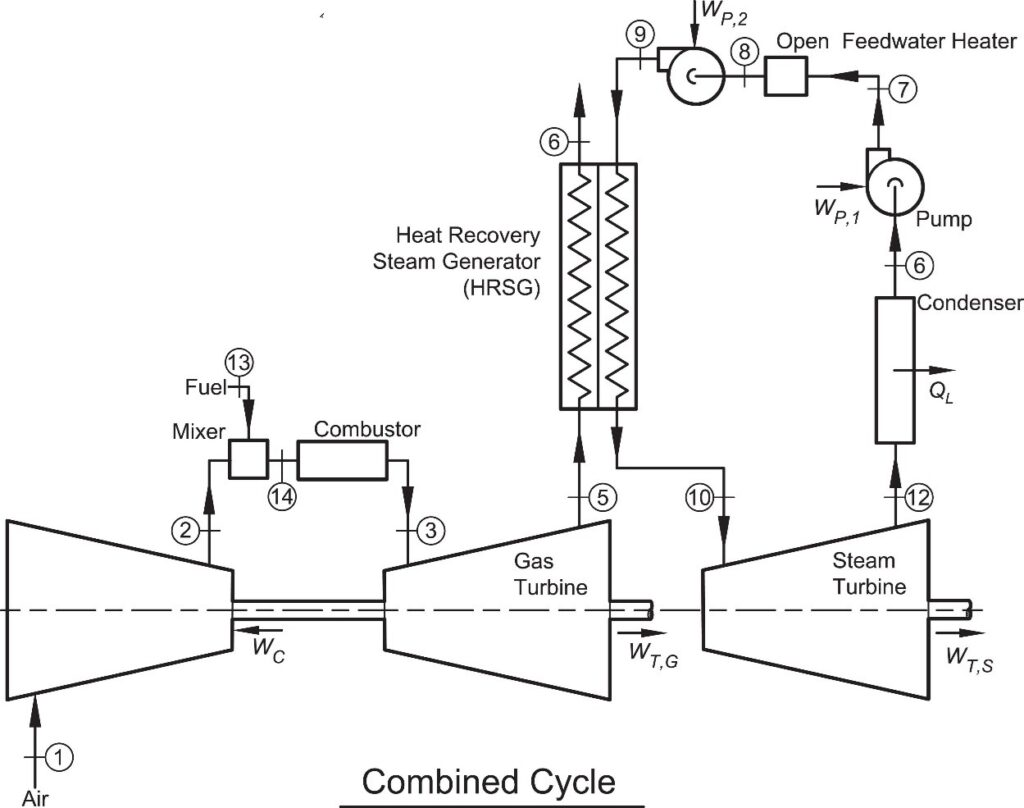

② SNT Energy: The Hidden Essential (Pick & Shovel) Global top-tier in Heat Recovery Steam Generators (HRSG) and Air-Cooled Heat Exchangers (ACHE) with approximately 40% market share in air-cooled systems. Whether it is gas turbines or SMRs, demand mechanically surges as more power plants are built. Air-cooled heat exchangers are especially critical in water-scarce regions like Texas and the Middle East.

③ Eaton (ETN): The Backbone of Power Infrastructure A global leader supplying medium/low-voltage circuit breakers, switchgear, transformers, and distribution panels. A core beneficiary of the “power infrastructure CAPEX supercycle” regardless of generation type.

6. Investment Priorities: Where Policy, Reality, and Narrative Intersect

Now for the deeper analysis. Having studied companies across the timeline and generation types, where is capital realistically concentrating as of January 2026?

- Now ~ 5 Years: Gas powers AI (earnings and CapEx exploding now). Solar and BESS provide backup.

- 5-10+ Years: Nuclear/SMR begins replacing gas (the central axis of the long-term structural story).

(Detailed core insights are available separately in my premium report.)

This is the energy war map I’ve meticulously drawn from Florence for 2026.

I hope this serves as a meaningful compass for reviewing your investment scenarios. For specific investment strategies and my Top Picks not fully covered here, please refer to my premium report at the link below. And if you have questions about the above content, please feel free to leave them in the comments!

[Global In-depth Report by Growth Papa]

[Disclaimer] This article provides investment perspectives, not specific buy/sell recommendations. Investment responsibility lies with the individual.

#AIPower #GasTurbines #ESS #SMR #EnergyInfrastructure