The Korea Export Data Dec 2025 report has been released, confirming South Korea’s role as the “canary in the coal mine” for the global economy. Serving as a critical leading indicator of worldwide economic health. In fact, it is remarkable that a government department works dedicatedly enough to release the previous month’s full data on the very first day of the following month.

I have analyzed the fresh sector-by-sector trends for December 2025, released on January 1st. This data serves as a vital benchmark for investment decisions in both Korea and the global market for the year ahead.

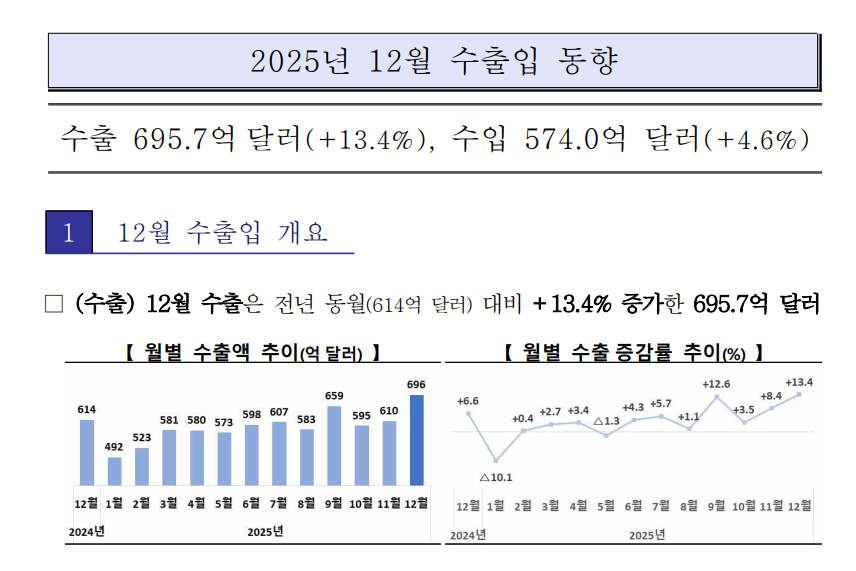

1. Korea Export Data Dec 2025 Review: Look Beyond the Total to See the “Acceleration”

In 2025, South Korea’s exports reached $709.7 billion (+3.8%), breaking the $700 billion mark for the first time in history. The trade surplus also recorded $78 billion, the largest since 2017, demonstrating the nation’s economic resilience.

However, smart investors should focus not on the “annual total,” but on the “year-end momentum.” December exports jumped 13.4% year-over-year to $69.6 billion. This represents the highest December performance on record, signaling that the growth engine heading into 2026 is accelerating.

2. Leading Sectors: Growth Proven by Numbers

Beyond simple base effects, these are the key sectors where structural demand explosions are being captured in the numbers.

① Semiconductors (+43.2%): The Undisputed Leader

Semiconductor exports surged 43.2% year-over-year in December, recording $20.8 billion. This marks the highest monthly performance ever.

Price Trends: Fixed prices for both DRAM and NAND are maintaining upward momentum. We are witnessing a “best-case scenario” where both volume (Q) and price (P) are rising simultaneously.

Investment Point: AI server demand is cascading down to general servers, maintaining a state of “excess demand.”

② Computers/SSD (+36.7%): The Hidden AI Beneficiary

While moving in tandem with semiconductors, the growth rate here is even steeper. Exports of computer products increased by 36.7% in December.

Notable: SSD exports alone grew 43.4% YoY. As long as AI infrastructure investment persists, this will remain a strong momentum driver throughout 2026.

Investment Point: As Big Tech companies expand AI data center CAPEX, demand for enterprise high-capacity SSDs (Solid State Drives) has exploded.

③ Power Equipment (+11.1%): The Hidden Arteries of the AI Era

This sector is inextricably linked to AI growth. December electrical equipment exports reached $1.57 billion (+11.1%), setting a new December record.

Investment Point: AI data centers are massive power consumers. Driven by this demand, annual exports for transformers and power equipment hit a record $16.7 billion. Combined with the global replacement cycle for aging power grids, the sector has entered a structural super-cycle.

④ Wireless Communication Devices (+24.7%): A Spectacular Revival

After a quiet period, wireless communication equipment showed a clear recovery with 24.7% growth in December.

Investment Point: Exports of finished goods, led by premium models like foldable phones, posted triple-digit growth (+178.4%), driving overall performance. This suggests the arrival of a hardware replacement cycle triggered by the launch of on-device AI phones.

⑤ Bio-Health & Cosmetics: Expanding K-Competitiveness

Beyond IT, sectors demonstrating structural growth are equally notable.

Cosmetics (+22.3%): The global popularity of K-Beauty shows no signs of cooling. December performance set a new all-time high, proving that indie brands and ODMs are successfully penetrating global markets beyond major conglomerates.

Bio-Health (+22.4%): CMO (Contract Manufacturing Organization) order backlogs are now shipping in earnest, fueling double-digit growth.

3. A Critical Perspective: Good Numbers, But “Separate the Wheat from the Chaff”

Strong data does not guarantee that all stocks will rise. A deep dive into the December data reveals signals that require caution and cold-headed interpretation.

- Automobiles (-1.5%): While achieving the highest annual performance in history, December saw slight negative growth. Hybrid vehicles (+53.8%) performed well, defending profitability, but uncertainties remain regarding the “EV Chasm” (demand slowdown) and potential US tariff policies.

- Secondary Batteries (-12.8%): Exports continued to decline due to falling Average Selling Prices (ASP) following mineral price drops and temporary stagnation in the EV market. A conservative approach is advised until clear rebound signals emerge.

- Shipbuilding (-2.0%): December figures dipped slightly, but this is a temporary fluctuation due to delivery schedules. Annual growth stood at +24.9%, and the delivery cycle for high-value vessels (such as LNG carriers) secured in previous orders will begin in earnest from 2026.

2026 Leading Sector Map

The direction indicated by export data is clear, but expectations are already priced into many stocks. Selective approaches are needed for companies with valuation concerns. (Note: This is for screening purposes only, not investment advice.)

| Sector | Core Theme | Potential Leading Companies (Korea/Global) | Investment Points |

|---|---|---|---|

| Semiconductors | AI Memory | Samsung Electronics, SK Hynix, Micron | Monopolistic supply of AI server essentials: HBM, DDR5, high-capacity eSSD |

| Semiconductors | Advanced Packaging | Hanmi Semiconductor, EOTechnics, Leeno Industrial | Increased demand for HBM manufacturing bonding equipment and high-performance test sockets |

| Power Equipment | Grid Super-cycle | LS ELECTRIC, HD Hyundai Electric, Sanil Electric | Benefits from North America/Europe grid replacement and data center power supply shortages, ESS demand expansion |

| Cosmetics | Indie/ODM | Silicone2, Cosmax, Kolmar Korea | Global penetration rate expansion and indie brand growth |

| Computers | Enterprise SSD | SK Hynix (Solidigm), SanDisk | Expanding market dominance in ultra-high-capacity SSDs for AI data centers |

| Automobiles | Hybrid/Parts | Hyundai Motor, Kia | Hybrid (HEV) mix improvement and high-value electronic component expansion |

| Shipbuilding | LNG/Special Vessels | HD Korea Shipbuilding & Offshore, Samsung Heavy Industries | Increased delivery volumes in 2026-27 and reflection of high-value LNG/offshore plant orders |

| Bio | CDMO | Samsung Biologics, Celltrion | Full-scale shipment of global big pharma contract production volumes and biosimilar expansion |

| IT Equipment | On-device AI | Samsung Electronics (MX), Samsung Electro-Mechanics, KH Vatec, FineMTech | Galaxy S26 AI phone launch and related high-performance component (MLCC, camera) demand |

Closing Thoughts

Looking ahead to 2026, the market is flooded with various predictions and rosy forecasts.

However, as an export-driven economy, South Korea’s performance is most fundamentally supported by hard numbers. I hope this analysis of monthly export-import data serves as a solid benchmark for you to carefully separate the wheat from the chaff among KOSPI and KOSDAQ companies, helping you build a robust and resilient portfolio for 2026.

This post is based on the Ministry of Trade, Industry and Energy’s “2025 Annual and December Export-Import Trends” press release and market analysis.