March 16, 2025 | by growth-papa

As of March 2025, silver prices have breached $34 per ounce, capturing the undivided attention of investors. With the global economy laser-focused on power generation, AI, and electric vehicles (EVs), silver demand is exploding while the supply deficit continues to deepen.

Today, I will delve into why I chose to invest in Silvercorp Metals Inc. (SVM) among various silver miners, focusing specifically on the outlook for supply shortages and industrial applications.

The Global Economy and the Rise of Silver

In March 2025, the world is shifting rapidly. China and Europe are concentrating on economic stimulus, while the U.S. is pushing for economic and security realignment under the Trump administration. Amidst this, the solar, AI, and EV industries have already seen rapid growth, but China’s economic stimulus is expected to send silver demand soaring even further.

- Solar Power: China produces over 70% of the world’s solar panels. Approximately 20kg of silver is required per 1MW of panels.

- AI: Silver’s high conductivity is essential for data centers and semiconductor chips. Power demand for data centers is projected to exceed 1,000 TWh in 2025 (BofA Global Research, 2024).

- EVs: Each vehicle uses 25–50g of silver. With sales expected to reach 18 million units in 2025, demand is projected to be around 560 tons.

- Precious Metals: Along with gold, silver serves as an inflation hedge, with increasing demand from both central banks and individual investors.

The problem lies in supply. Global silver production in 2024 was approximately 820 million ounces, but demand exceeded this figure. The deficit is expected to persist in 2025. Silver prices have jumped from the $31–32 range to $34 last week, and experts are predicting a breakout above $40.

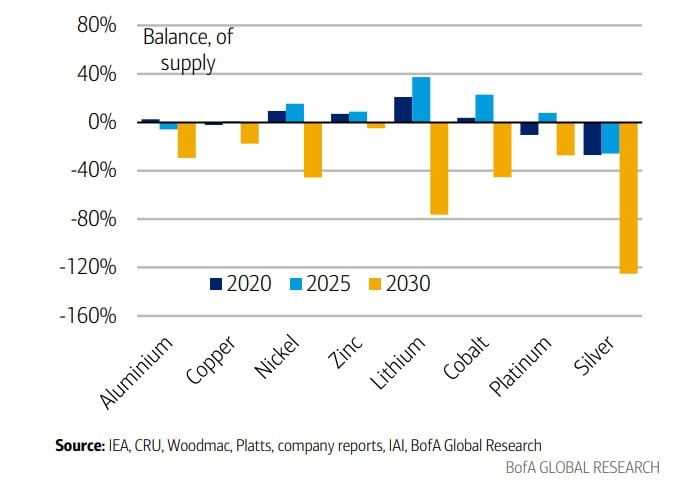

Visualizing the Silver Supply Crunch

Looking at the mineral supply-demand chart for 2020–2030 from BofA Global Research (2024 Report), the shortage of silver is stark:

- 2020–2025: Demand is already exceeding supply by 40%.

- 2030 Forecast: The deficit is expected to worsen to 120%.

This is far more severe than the projected deficits for Copper (-20%) or Lithium (-80%). It is the result of surging demand from Solar, EVs, and AI colliding with supply constraints. With the likelihood of a supply increase within the next 5 years being low, upward pressure on silver prices is intensifying.

Supply-Side Constraints: No Easy Solution

Silver is primarily obtained as a byproduct of copper, lead, and zinc mining, making it difficult to ramp up supply independently.

- Lack of New Mines: Delayed by long development cycles (7–10 years) and strict ESG regulations.

- Decline in Existing Mines: Production is decreasing in South America (Peru, Mexico) due to environmental regulations and falling ore grades.

- Recycling Limits: Recovery rates in 2023 were less than 20% of demand.

Conclusion: The supply shortage is highly likely to persist until 2030.

Why SVM Among Silver Miners?

Silvercorp Metals (SVM) is a Canada-headquartered mining company with a focus on silver, producing silver, lead, and zinc primarily from the Ying Mining District in China. Here is why it stands out compared to competitors like FSM, HL, and CDE.

1. Direct Link to Chinese Industrial Demand With mines located in China, SVM can directly reflect the local boom in Solar, EVs, and AI. Given that China is the global manufacturing hub, SVM appears more advantageously positioned than FSM (Mexico), HL (North America), or CDE (North America/Mexico).

2. Production Structure and Profitability SVM produces approximately 6.5 to 7 million ounces of silver annually, generating 30–40% of its revenue from silver. While Lead (40–50%) accounts for a significant portion, a 10% rise in silver prices is estimated to increase revenue by 3–4%, creating a strong leverage effect on EPS.

3. Geopolitical Positioning As a Canadian-headquartered company, it has some distance from U.S. sanctions. Trump’s tariffs are likely to have a greater impact on North American-based competitors (FSM, HL, CDE). However, operations within China do carry risks associated with U.S.-China tensions.

4. Competitor Comparison To see SVM’s appeal more clearly, I compared it with major peers:

- First Majestic Silver (FSM): Mexico-based. Strong silver focus but distanced from Chinese demand.

- Hecla Mining (HL): North America-focused. Stable, but low connectivity to China.

- Coeur Mining (CDE): High reliance on gold, limiting the benefits from a silver rally.

Ultimately, I view SVM as capable of directly benefiting from Chinese demand, maintaining cost efficiency, and showing superior revenue/profit growth due to its sensitivity to silver prices—assuming China’s stimulus successfully drives strong demand.

Investment Opportunities in the Era of Silver Shortage: SVM vs. ETF vs. Physical Silver

If the silver supply shortage persists, price increases are expected. Here are the investment options:

1. Silver Mining Stocks (SVM)

- Pros: Potential for margins to increase by 50%+ if silver rises 20%; reflects Chinese demand.

- Cons: Operational risks; impact of U.S.-China conflict (potential 20–30% production cut).

2. Silver ETFs (SLV)

- Pros: 1:1 tracking of futures prices; high liquidity.

- Cons: No leverage effect; rollover costs.

3. Physical Silver

- Pros: Inflation hedge; stability of physical assets.

- Cons: Storage costs; low liquidity.

I have chosen silver miners, specifically SVM. This is because I expect China’s Solar, AI, and EV industries to grow by another 20–30% in 2025, and SVM is positioned to capture this growth directly.

Closing Thoughts

2025 is highly likely to mark the opening of the “Era of Silver.”

My investment thesis is that SVM could emerge as a key beneficiary as the supply deficit (-120% by 2030 per BofA) intersects with Chinese industrial demand. I am taking a somewhat aggressive position to anticipate strong leverage effects as silver prices rise.

Of course, deepening U.S.-China conflicts and silver price volatility are variables to watch carefully. Believing in China’s economic growth and the era of silver shortage, I expect SVM to stand at the center of this trend.

I anticipate holding this position for perhaps 1 to 2 years.

2025년, SVM(Silvercorp Metals)이 주목받는 이유: 은의 공급 부족 시대와 투자 기회

2025년 3월, 은 가격이 온스당 34달러를 돌파하며 투자자들의 시선을 사로잡고 있다. 글로벌 경제가 전력, AI, 전기차에 몰두하면서 은 수요가 폭발적으로 늘고, 공급 부족은 갈수록 심화되고 있다. 오늘은 은 광산 기업 중 나는 왜 SVM(Silvercorp Metals Inc.)에 투자 했는지, 특히 공급 부족 전망과 산업 활용을 중심으로 파헤쳐 보려 한다

글로벌 경제와 은의 부상

2025년 3월, 세계는 급변 중. 중국과 유럽은 경기 부양에 힘쓰고, 미국은 트럼프 주도의 경제·안보 재편을 추진 중이다. 이런 가운데 이미 태양광, AI, 전기차 산업이 급성장했지만 중국의 경제부양이 은 수요를 더 치솟게 할 예정이다.

- 태양광: 중국은 세계 태양광 패널의 70% 이상을 생산하며, 패널 1MW당 20kg의 은이 필요.

- AI: 데이터센터와 반도체 칩에서 은의 전도성이 필수적. 2025년 데이터센터 전력 수요는 1,000TWh를 넘을 전망(BofA Global Research, 2024).

- 전기차: 차량 1대당 25~50g의 은이 사용되며, 2025년 1,800만 대 판매로 약 560톤 수요가 예상.

- 귀금속: 금과 함께 인플레이션 헤지 수단으로, 중앙은행과 개인 투자 수요도 증가 중.

문제는 공급이다. 2024년 글로벌 은 생산은 약 8억 2천만 온스였지만, 수요가 이를 초과하며 2025년에도 부족이 지속될 전망이다. 은 가격은 현재 31~32달러에서 지난주 34달러로 뛰었고, 전문가들은 40달러 돌파를 예상하고 있다.

은의 공급 부족, 그래프로 확인

BofA Global Research(2024 보고서)의 2020~2030년 광물 공급-수요 그래프를 보면, 은의 부족이 두드러진다:

- 2020~25년: 수요가 공급대비 40%이미 부족한 상황

- 2030년: 120%까지 악화 전망.

구리(-20%), 리튬(-80%)보다 훨씬 심각한 수준이다. 태양광, EV, AI 수요 급증과 공급 제약이 맞물린 결과로, 5년 내 공급 증가 가능성은 낮아 은 가격 상승 압력이 커지고 있다.

공급 측 제약, 해결책은 요원

은은 주로 구리, 납, 아연 채굴의 부산물로 얻어져 독립적 공급 확대가 어렵다.

- 신규 광산 부족: 개발 주기(7~10년)와 ESG 규제로 지연.

- 기존 광산 감소: 남미(페루, 멕시코) 환경 규제로 생산량 감소, 채굴 등급 하락.

- 재활용 한계: 2023년 회수량은 수요의 20% 미만.

>>결론적으로, 2030년까지 공급 부족이 지속될 가능성이 높아 보인다.

SVM, 은광 업체 중 왜 특별할까?

SVM은 캐나다 본사를 둔 은 중심 광산 기업으로, 중국 내 Ying 광구에서 은, 납, 아연을 생산한다. 경쟁사(FSM, HL, CDE)와 비교해 보았다.

- 중국 산업 수요와의 직결성

SVM은 중국 내 광산으로 태양광, EV, AI 붐을 바로 반영할 수 있다. 중국이 글로벌 생산 허브인 점을 감안하면, FSM(멕시코), HL(북미), CDE(북미·멕시코)보다 유리해 보인다. - 생산 구조와 수익성

SVM은 연간 약 650만~700만 온스의 은을 생산하며, 수익의 30~40%를 은에서 얻는다. 납(40~50%)이 주 비중이지만, 은 가격 10% 상승 시 매출 3~4% 증가로 주당순이익(EPS)에 강한 레버리지 효과가 있다고 보인다 - 지정학적 위치

캐나다 본사로 미국 제재와 거리 있으며, 트럼프 관세가 북미 기업(FSM, HL, CDE)에 더 큰 영향을 줄 가능성이 높다. 다만, 중국 내 운영은 미중 갈등 리스크를 동반 한다.

경쟁사 비교

SVM의 매력을 더 명확히 보기 위해 주요 은광 업체와 비교해 봤

- First Majestic Silver (FSM): 멕시코 기반, 은 중심성이 강하지만 중국 수요와 거리 있음.

- Hecla Mining (HL): 북미 중심, 안정적이지만 중국 연계성 낮음.

- Coeur Mining (CDE): 금 의존도가 높아 은 상승 수혜가 제한적.

결국, SVM은 중국 수요를 직접적으로 받을 수 있고, 비용 효율성이 있으며, 은 가격 민감도에서 나타낼 매출/이익 상승에서 두각을 나타낼 수 있으리라 봤다. 물론 중국의 경제 부양 정책이 강한 수요를 이끌어 주리라는 기대와 전제 하에.

은 부족 시대의 투자 기회: SVM vs. ETF vs. 실물 은

은의 공급 부족이 지속되면 가격 상승이 예상된다. 투자 옵션은 다음정도..

1. 은광업 주식 (SVM)

- 장점: 은 가격 20% 상승 시 마진 50% 이상 증가 가능, 중국 수요 반영.

- 단점: 운영 리스크, 미중 갈등 영향(생산 20~30% 감소 가능성).

2. 금은 선물 ETF (SLV)

- 장점: 선물 가격 1:1 추종, 유동성 높음.

- 단점: 레버리지 효과 없음, 롤오버 비용 발생.

3. 실물 은

- 장점: 인플레이션 헤지, 실물 자산 안정성.

- 단점: 보관 비용, 유동성 낮음.

난 은광업체, 그 중에서 SVM을 선택했다. 중국 태양광/AI/EV 산업이 2025년에도 20~30% 성장할 것으로 보이고, SVM은 이를 직접 반영할 수 있기 때문이다.

마무리

2025년은 은 시대의 개막을 알릴 가능성이 커 보인다.

BofA 전망처럼 공급 부족(-120%)과 중국 산업 수요가 맞물리며, SVM은 주요 수혜자로 떠오를 수 있겠다는 것이 투자 아이디어다. 여기에 은 가격 상승 시 강한 레버리지 효과를 기대할 수 있어 다소 공격적인 투자를 해본다.

다만, 미중 갈등 심화나 은 가격 변동성은 주의해야 할 변수

중국 경제 성장과 은 부족 시대를 믿으며, SVM이 그 중심에 설 것으로 기대한다.

아마 1~2년은 가지고 있지 않을까.