Introduction: The Hidden Infrastructure of Smart Technology

As electronic devices become increasingly sophisticated—from electric vehicles and data centers to AI devices and robotics—there’s one tiny component that’s becoming absolutely essential: the Multi-Layer Ceramic Capacitor (MLCC).

While most investors focus on the flashy end products, I’ve discovered that the real opportunity lies deeper in the supply chain. After extensive analysis of the MLCC ecosystem, I ultimately chose Daeju Electronic Materials over industry giants like Samsung Electro-Mechanics and Murata Manufacturing. Here’s why.

Understanding MLCC: The Nervous System of Modern Electronics

What Makes MLCC Critical?

MLCC is essentially the “nervous system” of electronic devices. These rice-grain-sized components perform four critical functions:

- Voltage Stabilization: Cushions sudden voltage changes to protect circuits—crucial for AI semiconductors with rapidly fluctuating power consumption

- Noise Filtering: Removes electrical interference to enhance signal quality in high-precision sensors and communication equipment

- Signal Processing: Allows or blocks specific frequencies—increasingly vital for 5G/6G high-frequency communications

- Energy Storage: Provides instant power when needed during EV rapid acceleration or AI computational load spikes

The Structural Market Transformation

The MLCC market is undergoing a fundamental shift from commodity products to high-performance, premium segments:

| Market Segment | Traditional | New Growth Areas |

|---|---|---|

| Applications | Smartphones, PCs, Appliances | AI Servers, EVs, Data Centers |

| Growth Rate | 0-3% (saturated) | 15-25% (high growth) |

| Unit Price | $0.01-0.1 per piece | $0.5-5 per piece |

| Profitability | Low-margin, high-volume | High-margin, premium |

| Tech Requirements | Standard specs | Extreme specs (high temp/voltage) |

This isn’t just growth—it’s a P × Q expansion where both price (P) and quantity (Q) are increasing simultaneously.

The New Growth Drivers: AI, EVs, and Defense

AI Data Center Explosion

The scale of AI infrastructure investment is unprecedented:

- Microsoft: $80B in AI data centers (2025)

- Google: $75B investment planned

- Meta: $60B+ through 2025

Each AI server requires 3-5x more high-performance MLCCs than traditional servers due to:

- GPU power management (700W+ per NVIDIA H100)

- HBM (High Bandwidth Memory) noise control

- VRM (Voltage Regulation Module) stability

Electric Vehicle Revolution

The MLCC demand multiplication is staggering:

- ICE vehicles: ~3,000 MLCCs

- Hybrid vehicles: ~6,000 MLCCs (2x)

- Electric vehicles: 30,000+ MLCCs (10x)

But quantity isn’t the whole story. EVs demand extreme specifications:

- High voltage systems (800V → 1,200V)

- Battery management systems requiring hundreds of high-voltage MLCCs

- Inverter systems handling dozens of kW in harsh environments

- ADAS systems where reliability directly impacts human safety

Defense and Aerospace Surge

Post-Ukraine war, global advanced weaponry demand has exploded. Modern military systems require:

- Guided missiles with multi-sensor fusion

- Autonomous drones with real-time processing

- Phased array radars with thousands of modules

- Electronic warfare equipment with extreme EMI resistance

Military-grade MLCCs command 10-50x premium pricing due to extreme environmental requirements:

- Operating range: -40°C to +125°C

- Shock resistance: Thousands of G-force acceleration

- Long-term storage: 10+ years with immediate deployment capability

Why I Passed on the Obvious Choices

Samsung Electro-Mechanics: Growth Diluted by Legacy Business

While Samsung Electro-Mechanics shows impressive growth in premium MLCC segments, the reality check is sobering:

2024 Revenue Breakdown (~$8.2B total):

- MLCC: 40-50% (~$3.3-4.1B)

- Camera Modules: 33-38% (~$2.7-3.1B)

- FC-BGA: 15-18% (~$1.2-1.5B)

The dilution problem:

- AI server MLCC: Only 2-3% of total revenue

- Automotive MLCC: 8-10% of total revenue

- Total high-value exposure: Just 10-13% of business

Even if AI server MLCC grows 50% annually, it only contributes 1-1.5% to total company growth. The smartphone dependency remains significant across multiple business segments.

Murata Manufacturing: Market Leader Facing Headwinds

Murata, despite being the global MLCC leader with ~$15B revenue, faces structural challenges:

- Mobile dependency: Still 39% of revenue from smartphones

- 2025 outlook: -9% revenue decline expected

- Premium transition: Slower compared to Samsung Electro-Mechanics

Both manufacturers suffer from the same fundamental issue: High-value MLCC growth is meaningful but represents a small portion of their total business mix.

The Material Advantage: Why Daeju Electronic Materials

Positioned at the Value Chain’s Commanding Heights

In the MLCC value chain, materials suppliers hold unique advantages:

- Quality Determination: Core materials (ceramic powder, electrode paste, release film) fundamentally determine MLCC performance and pricing

- Supply Dependency: MLCC manufacturers are completely dependent on materials suppliers—no substitution possible during production

- Pricing Power: High barriers and limited suppliers enable materials companies to maintain pricing power

- Leverage Effect: When MLCC demand and pricing rise, materials suppliers capture amplified benefits

Daeju’s Dual Growth Engines

Engine 1: Electrode Paste Monopoly

- Domestic monopoly: Only supplier of MLCC electrode paste in Korea

- Critical component: Determines electrical reliability, voltage resistance, and miniaturization capability

- Customer lock-in: Samsung Electro-Mechanics, Samsung SDI, and other major clients are 100% dependent

- Premium pricing: AI/automotive/defense MLCC electrode paste commands 5-10x pricing versus standard grades

Engine 2: Silicon Anode Materials Game-Changer

- Revolutionary performance: 11x capacity density vs. traditional graphite (4,200 mAh/g vs. 372 mAh/g)

- Tesla breakthrough: Supplying Panasonic for Tesla Model Y and Model 3 vehicles since mid-2025, replacing Chinese BTR

- IRA policy winner: Korean company benefiting from U.S. policy to exclude Chinese battery materials

- Technical moat: CVD-based SiOx composite technology with proven mass production capability

The Numbers Don’t Lie

Revenue Concentration in High-Value Segments:

- Electrode paste: ~40% of revenue (premium pricing, monopolistic position)

- Silicon anode: ~30% of revenue (explosive growth potential)

- Combined: 70% of business focused on ultra-high-value applications

Compare this to Samsung Electro-Mechanics’ ~10-13% high-value exposure.

Growth Trajectory:

- 2025E: 17-19% revenue growth

- Operating margin: 8.8-13.4%

- ROE: 12-16.8%

Investment Thesis: Leveraged Play on Structural Transformation

The Leverage Multiplier

When Samsung Electro-Mechanics grows its premium MLCC business by X%, Daeju Electronic Materials benefits by 1.5-2X due to:

- Higher material content ratio in premium MLCCs

- Price elasticity favoring specialized suppliers

- Operating leverage from fixed cost base

Timing the Inflection Point

Currently experiencing “trickle-down delay” where Samsung’s MLCC growth hasn’t fully reflected in Daeju’s results yet. This creates a temporary disconnect offering attractive entry timing.

Expected catalysts for 2025 H2:

- Samsung’s Busan automotive-dedicated production line full ramp

- New high-performance electrode paste product certifications

- Tesla volume expansion through Panasonic supply chain

Long-term Structural Advantages

Defensive moats:

- Patent portfolio in metal nanopowder synthesis

- Customer qualification cycles (2-3 years typical)

- Integrated supply chain from raw materials to finished products

Offensive opportunities:

- U.S. IRA policy creating permanent Chinese supplier exclusion

- Global OEM diversification reducing China dependency

- Technology leadership in next-generation battery materials

Valuation and Investment Outlook

Current Valuation Reality

At ₩70,700 per share:

- Forward P/E: 32x

- EV/EBITDA: 25.4x

This already reflects significant growth expectations. The market has priced in the structural transformation story, making execution critical for returns.

12-Month Forward Scenarios

Based on Tesla ramp-up and Samsung premium MLCC acceleration:

| Scenario | Target Multiple | Upside Potential |

|---|---|---|

| Conservative | 25x EV/EBITDA | -2% |

| Base Case | 28x EV/EBITDA | +13% |

| Optimistic | 30x EV/EBITDA | +22% |

2027 Vision: When the Story Matures

Projected fundamentals:

- Revenue: ₩537.5B (vs. ₩200-240B in 2025)

- Operating margin: 15% (scale economics)

- EPS: ₩3,820 (vs. ₩2,200 forward)

At this scale, valuation would normalize to 18-20x P/E, requiring continued stock appreciation to maintain reasonable multiples.

Risk Factors and Mitigation

Key Risks

- Execution risk: High growth expectations leave little room for disappointment

- Customer concentration: Heavy dependence on Samsung ecosystem

- Technology risk: Potential disruption in MLCC or battery technologies

- Valuation risk: Currently priced for perfection

Why These Risks Are Manageable

- Proven track record: Already supplying global OEMs (Tesla, Porsche, LG Energy Solution)

- Diversification progress: Expanding beyond Samsung to global customers

- Technology leadership: Continuous R&D investment maintaining competitive edge

- Market structure: Oligopolistic supply structure provides pricing stability

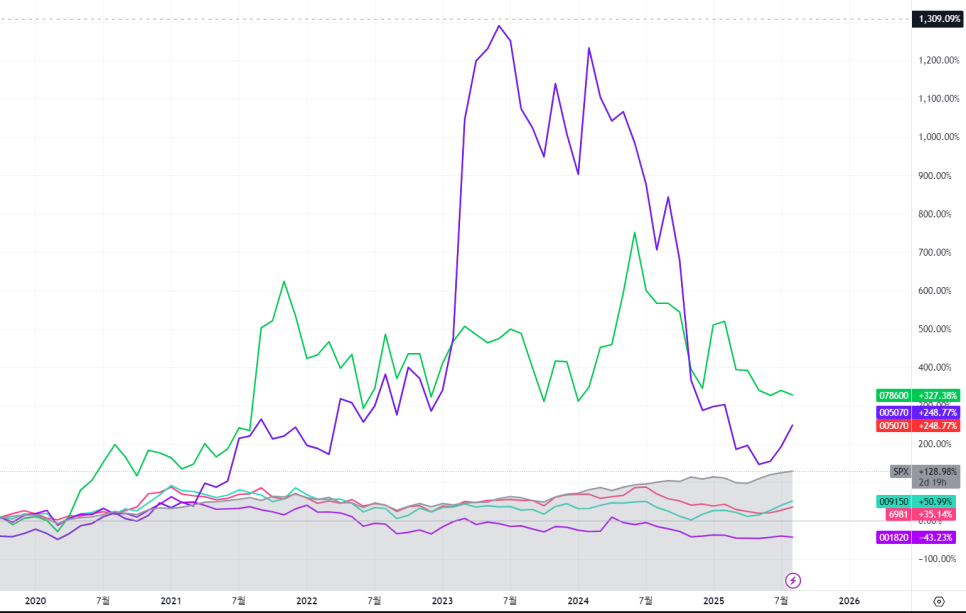

Green: Daeju Electronic Materials, Purple: Cosmo Advanced Materials

Other companies (Samsung Electro-Mechanics/Murata Manufacturing/Samhwa Capacitor) are underperforming the S&P 500.

Conclusion: Conviction and Patience

Why Daeju Electronic Materials over the obvious choices:

- Concentration advantage: 70% revenue exposure to ultra-high-growth segments vs. 10-13% for manufacturers

- Leverage multiplier: Benefits from MLCC growth at 1.5-2x rate

- Dual growth engines: Electrode paste monopoly + silicon anode breakthrough

- Policy tailwinds: IRA and Korean materials independence policies

- Execution visibility: Tesla supply chain entry validates technology and market position

The investment requires two things:

- Conviction in the structural transformation of electronics toward higher performance and efficiency

- Patience to wait for the trickle-down effects to materialize in financial results

While the current valuation reflects high expectations, the combination of monopolistic positioning, dual growth engines, and structural market transformation creates a compelling risk-adjusted opportunity for investors willing to look beyond the obvious choices.

The best investments often hide in plain sight—not in the companies everyone talks about, but in the specialized suppliers that make those companies’ success possible.

Disclaimer: This analysis is for educational purposes only and should not be considered as investment advice. Past performance does not guarantee future results. Please conduct your own research and consult with financial advisors before making investment decisions.