Today, I’m looking back at the investment ideas I shared with friends on January 2nd and March 7th, 2025, to see how they’ve evolved over the past few months.

From early on, I anticipated capital flows toward emerging markets, but Trump’s uncertainty seemed to create a prolonged effect of capital being trapped in US-focused investments. Will this now shift toward full-scale movement? I’d bet against Trump allowing that. While there’s short-term uncertainty, I believe he’ll steadily drive toward “Great America Again” within limits that don’t fundamentally impact fundamentals. Of course, emerging market investments remain valid.

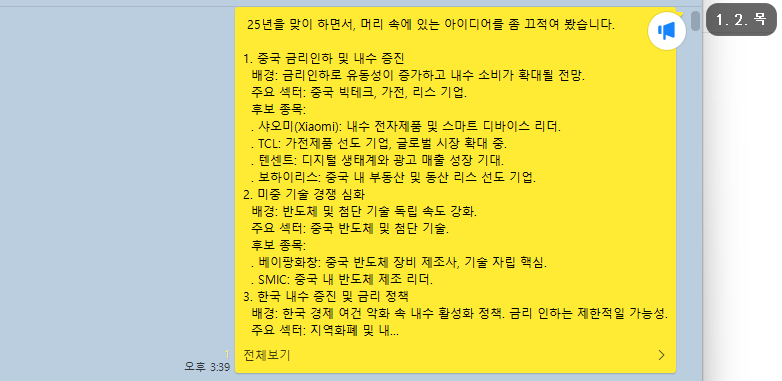

January 2nd Ideas

1. China Interest Rate Cuts and Domestic Stimulus

- Background: Liquidity increase from rate cuts expected to expand domestic consumption

- Key Sectors: Chinese big tech, home appliances, leasing companies

- Target Stocks: Xiaomi (domestic electronics and smart devices leader), TCL (leading home appliance company expanding globally), Tencent (digital ecosystem and advertising revenue growth expected), Bohai Leasing (leading real estate and equipment leasing in China)

2. Intensifying US-China Tech Competition

- Background: Accelerated semiconductor and advanced technology independence

- Key Sectors: Chinese semiconductors and advanced technology

- Target Stocks: Naura (Chinese semiconductor equipment manufacturer, core of tech independence), SMIC (China’s semiconductor manufacturing leader)

3. Korea Domestic Stimulus and Interest Rate Policy

- Background: Domestic activation policies amid deteriorating Korean economic conditions. Interest rate cuts likely limited

- Key Sectors: Local currency and domestic consumption activation companies

- Target Stocks: KONA I (key technology company related to local currency), BGF Retail (direct beneficiary of domestic consumption expansion)

4. European-Chinese Liquidity Effects and Consumption Growth

- Background: Expected increase in luxury consumption from European and Chinese rate cut effects

- Key Sectors: Luxury goods, home appliances

- Target Stocks: LVMH, Hermès (sustained global luxury consumption growth), TCL (strengthening role in global home appliance market after Samsung/LG)

5. European Military and Aerospace Investment

- Background: Strengthened EU military spending and aerospace investment

- Key Sectors: Defense industry and aerospace

- Target Stocks: Safran (aviation engine and aerospace systems leader), Airbus (core of European aerospace industry)

6. European AI and Digital Transformation Investment

- Background: Expanded AI, digital twin, cloud investment

- Key Sectors: Software, digital twin

- Target Stocks: SAP (core of European software and cloud investment), Siemens (digital twin technology leader)

7. NVIDIA Benefits and Semiconductor Manufacturing

- Background: Increased global semiconductor demand from strengthened NVIDIA investment

- Key Sectors: Taiwan semiconductors and electronics manufacturing

- Target Stocks: TSMC (core of global semiconductor production), MediaTek (smart devices and IoT market expansion)

8. AI Convergence with Autonomous Driving and Robotics

- Background: Tesla maintaining leadership in autonomous driving and robotics with accelerated global investment in related industries

- Key Sectors: Autonomous driving, robotics, AI solutions

- Target Stocks: Tesla (strengthening global leadership through autonomous driving technology and Optimus robot project), NVIDIA (core role in technical support through autonomous driving AI platforms and GPUs), Hyundai Motor (potential attention from Boston Dynamics IPO possibility or related news), XPeng (strengthening position in Chinese autonomous driving technology and EV market), Rainbow Robotics (growth potential highlighted with robotics technology capabilities, Samsung Electronics acquisition possibility)

March 7th Ideas

By March, Trump’s policies became more concrete, leading to updated ideas. While emerging market ideas remained valid, emerging market recovery was slower than expected due to Trump-related uncertainty. However, ideas related to power, defense, and US-China tech competition showed good performance.

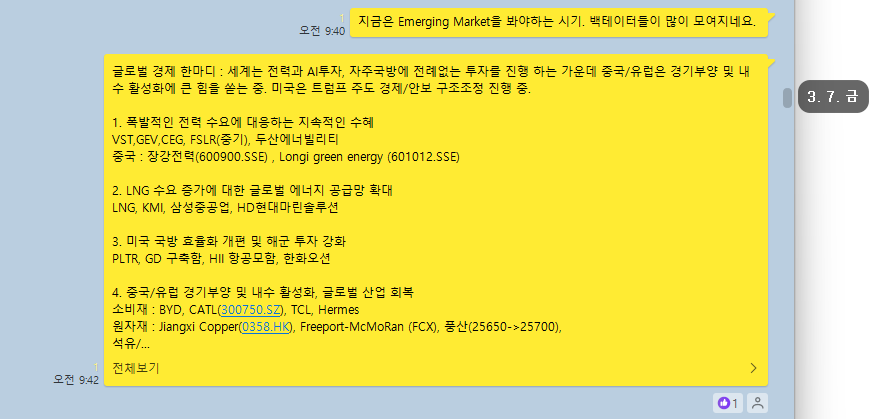

1. Sustained Benefits from Explosive Power Demand

VST, CEG, BWXT, PWR, GEV, Doosan Enerbility China: Changjiang Power (600900.SSE), Longi Green Energy (601012.SSE)

2. Global Energy Supply Chain Expansion from Increased LNG Demand

LNG, Samsung Heavy Industries, HD Hyundai Marine Solution

3. US Defense Efficiency Reform and Naval Investment Strengthening

PLTR (AI-based), CRWD (cybersecurity), KTOS (drone/unmanned systems), GD (destroyers), HII (aircraft carriers), Hanwha Ocean

4. China/Europe Economic Stimulus and Domestic Activation, Global Industrial Recovery

- Consumption: BYD, CATL (300750.SZ), TCL, Hermes, JD, Tencent (700.HK)

- Raw Materials: Jiangxi Copper (0358.HK), Freeport-McMoRan (FCX), Poongsan

- Oil/Chemicals: LG Chem

- Capital Investment: Siemens, Linde

5. Advanced Technology Self-Sufficiency Acceleration from Intensifying US-China Tech Competition

Naura (002371.SZ), SMIC (688981.SH), AMD

6. Strengthened European Military and Aerospace Investment

Safran, Rolls Royce, Rheinmetall, Hanwha Aerospace

7. Strengthened AI Systems and Data Center Investment in Europe, China, Korea

Alibaba, SAP, Douzone Bizon, Veritone

8. Realization of Humanoid Robots and Autonomous Driving

NVIDIA, Tesla, Xiaomi, XPeng, BYD, UBTech Robotics

9. Increased Volatility from Trump-Led Economic/Security Restructuring

VIXM, TLT (20-year), IEF (7-10 years), SVM (Canadian silver mining company based in China)

10. Korean Wave Riding the Spring Wind

HYBE, CJ ENM, Timefolio K Culture Active ETF

Key Company Performance (January 2 → August 26)

Doosan Enerbility (250.5% return) – Maximum beneficiary of nuclear power and electrical infrastructure

18,060 → 63,300 KRW The ultimate beneficiary where AI data center power demand and nuclear power revival acted synergistically. Explosive growth achieved through simultaneous expansion of SMR (Small Modular Reactor) technology capabilities and existing power plant maintenance business.

KTOS (155.7% return) – Reversal of drones and unmanned systems

26.38 → 67.47 USD Successfully reversed from initial struggles as the importance of drones became highlighted through the Ukraine war. Increased government contracts and surging demand for unmanned systems became growth drivers.

Rheinmetall (171.2% return) – European defense absolute leader

604.00 → 1,638.00 EUR Received maximum benefits among European defense companies from the Ukraine war. German government’s 100 billion euro defense budget increase and weapon orders from NATO member countries poured in, recording the highest order backlog in history.

Hanwha Ocean (190.2% return) – Core of naval power enhancement

37,800 → 109,700 KRW Achieved explosive growth through Korea Navy’s next-generation destroyer (KDDX) project and overseas order expansion. Particularly leaped to become a global defense company through Polish submarine exports and Australian naval vessel project participation.

XPeng (109.2% return) – Dark horse of Chinese autonomous driving

45.00 → 94.15 HKD Successfully differentiated through autonomous driving technology capabilities in the Chinese EV market. Particularly strengthened premium brand positioning through improved performance of urban autonomous driving function ‘XNGP’.

SMIC (93.8% return) – Symbol of Chinese semiconductor independence

29.00 → 56.2 HKD Maximum beneficiary of US-China tech competition. SMIC achieved record highs by breaking through $2 billion in revenue for the first time in Q3 2024, expanding 12-inch wafer monthly production capacity and recording high utilization rates.

UBTech Robotics (78.5% return) – Rising star of Chinese robotics

53.00 → 94.60 HKD Rising star of the Chinese robotics industry. Accelerating global market entry based on humanoid robot and industrial robot technology capabilities.

Siemens (40.2% return) – Overcoming German manufacturing limitations

167.88 → 235.4 EUR Despite German economic downturn, showed steady growth through digital twin and industrial automation demand. Found new growth drivers through AI and IoT technology convergence.

Safran (34.4% return) – Composite growth of aviation and defense

214.9 → 288.9 EUR While civilian aircraft market recovery was slow, achieved steady results through increased orders in defense and aerospace systems. Particularly benefited from expanded European defense industry investment.

Xiaomi (57.4% return) – Representative of Chinese domestic market

34.00 → 53.50 HKD Benefited from Chinese domestic stimulus. Smartphone market recovery, IoT ecosystem expansion, and launch of EV SU7 acted synergistically.

Relatively Disappointing Stocks

VST (27.5% return) – Power infrastructure adjustment

149.0 → 190.0 USD Benefited from increased AI data center power demand but stock was adjusted due to poor Q2 performance. Long-term growth prospects remain bright due to power grid modernization demand.

CEG (27.9% return) – Nuclear renaissance delay

242.6 → 310.4 USD Despite nuclear power revival attention, new project progress was slow due to regulatory approval delays and rising construction costs.

LG Chem (20.0% return) – Chemical industry benefits from Chinese consumption recovery

242,500 → 291,000 KRW Expected chemical raw material and material demand to increase from China’s economic stimulus policies and manufacturing recovery, but this was much slower than anticipated. We continue to expect this going forward.

Hermès (-8.9% return) – Luxury consumption contraction

€2,301 → €2,096 Despite Chinese economic stimulus, luxury consumption recovery is delayed. Consumption pattern changes (small confirmed happiness, character accessories popularity, etc.) and reduced overseas travel had impacts.

Conclusion: The Power of Investment That Captures Structural Changes

This review reconfirmed that capturing themes at important technological, social, and cultural inflection points early allows their validity to persist over time and generate above-expected returns.

Mega trends like AI power infrastructure, defense industry from geopolitical tensions, US-China tech competition, and autonomous driving technology were not merely temporary phenomena but starting points of structural changes.

Investment is ultimately a continuous process of hypothesis testing about the future. While we didn’t achieve perfect returns in every stock, we maintained unwavering investment principles within the big flow and achieved overall above-expected performance. What’s important is not the success or failure of individual stocks, but reading the essence of epochal changes and executing consistent investment philosophy accordingly.

Most stocks currently showing relatively disappointing returns still have valid investment ideas, but the timing is often later than expected.

As André Kostolany said, in investing “2+2=4” doesn’t apply, but rather “2+2=5-1”. Even with detours, ultimately correct investment ideas are proven by time – a point confirmed once again.

As the pace of change accelerates, such long-term thinking and patience from a structural perspective will become even more important.

Going forward, I’ll post updates every three months to check important change flows of our times.