Recent volatility in technology stocks has made the tech rally that has led markets since April feel less comfortable for investors. While the influence of semiconductors and technology companies driving AI transformation will continue, it feels like a correction is approaching. Trump’s imposition of semiconductor tariffs and the push for “Made in USA” vertical integration in advanced industries – not just design capabilities but manufacturing as well – seems to be intensifying.

Although the United States has traditionally valued corporate autonomy and efficiency as paramount values in capitalist development, it is now creating a flow that domestic companies must follow by directly linking technology, industry, energy, and pharmaceuticals to national security. The industrial and corporate trends that once focused on efficient production according to Ricardo’s theory of comparative advantage will now see their future prospects change based on whether manufacturing plants are located in the United States or not.

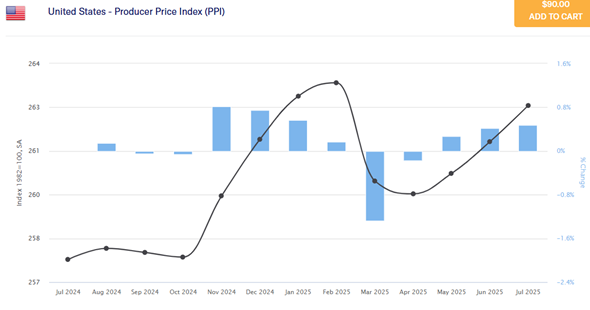

Regarding U.S. inflation and Fed policy rates that the global economy is watching, despite July PPI rising 0.9% monthly, significantly exceeding market expectations of 0.2%, securities markets remained solid. This seems to reflect market expectations that companies will absorb producer price increases rather than pass them on to consumers (Trump’s corporate tax cuts also play a role). Long-term bonds were not significantly affected either, suggesting the market still views inflation as controllable and focuses only on CPI + unemployment rate results themselves. Looking at securities flows, there doesn’t seem to be much skepticism about rate cut plans at the September FOMC.

Trade with China, a trading partner that could directly impact U.S. inflation, continues to decline in scale, but appears to be managed to avoid unnecessary inflationary stimulus. The U.S. government seems to always respond seriously to trade negotiations with the Chinese government, and this time a 3-month extension was granted. While conflicts may intensify, the U.S. government’s true intention appears to be that it cannot actually implement large-scale tariffs.

Considering these macro variables, funds seem likely to flow toward defensive sectors with high growth potential (communications, healthcare) that are less exposed to macro volatility before the September FOMC, and this trend already appears to be visible. Depending on FOMC results, market flows may change again, centering on growth stocks or interest rate-sensitive stocks.

Key Macro Checks

Real M2

The Fed’s QT (quantitative tightening) is complete, and gradual QE is underway. Nothing bad for the stock market.

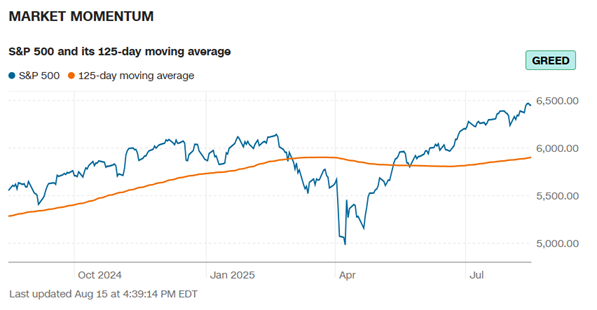

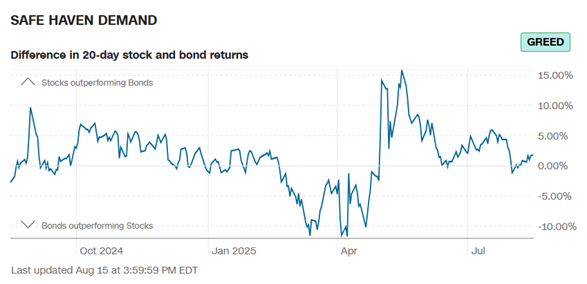

Fear and Greed Check

Based on the 125-day moving average, it has risen considerably compared to the past. The momentum is very good. It wouldn’t be strange if the momentum breaks or continues.

The yield difference between stocks and bonds shows stocks are still preferred. While we haven’t entered bond territory yet, we’ve gotten quite close. From this perspective, preference for defensive assets seems natural.

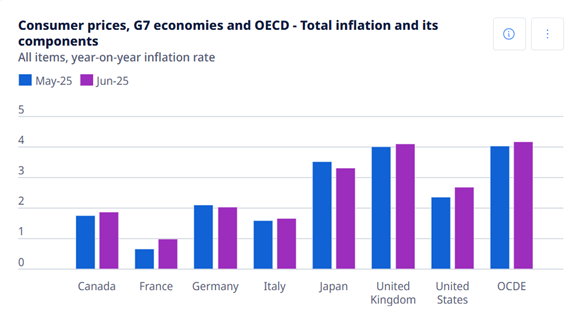

Country-by-Country CPI/CCI Trends and Bond Developments

CCI: Korea > Germany > China > USA in terms of consumer evaluation of future economic trends. The U.S. deteriorated significantly due to tariff effects but is on a recovery trend.

CPI: USA > Germany > Korea > France > China, but all countries maintain healthy 1-2% levels without notable increases or decreases.

China stands out – looking at YoY inflation, it appears to be overcoming deflation and creating an inflationary atmosphere. This should positively impact the global economy.

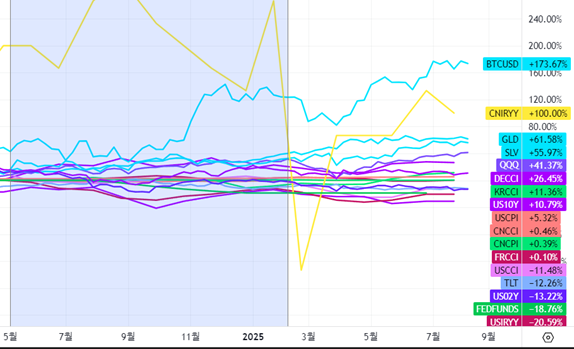

Bond Trends

U.S. 10-year Treasury rates show no signs of significant decline. 2-year rates have come down considerably and are maintaining their trend.

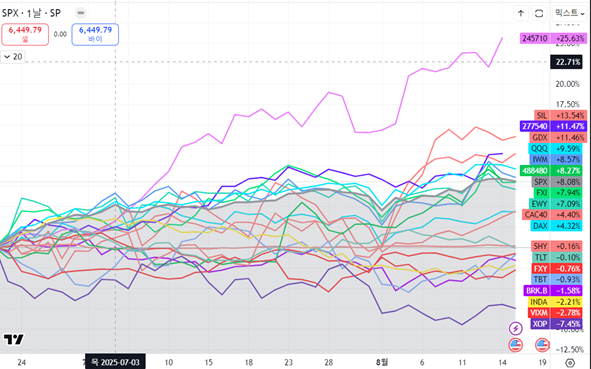

Major Country/Asset Performance Trends

Vietnam > Korea > Nasdaq > Silver > Russell > Oil > China > Japan > Germany > France > TBT > SHY > Gold > TLT > India > Berkshire

Funds are clearly flowing into emerging markets, with concentration in Vietnam and Korea. Could China be next? A point to watch.

For gold and silver, while only silver rose in the short term, expanding to May 2024 shows they outperformed stocks and continue to record the highest returns among assets. Recent silver trends have caught up with gold, likely due to recognition of both silver’s industrial demand from global economic recovery and its value as a safe asset. (Silver and platinum have industrial demand as conductors and catalysts, respectively)

The market is channeling funds toward emerging market growth while not delaying preference for safe assets due to U.S. policy uncertainty. Investment flows to gold/silver rather than bonds.

Recent Key Indicators: July PPI

I wanted to analyze CPI transmission risks by sector. While many B2C companies could theoretically pass on CPI costs, the market consensus seems to be that they won’t transmit costs in the short term due to competitive intensity, government/social scrutiny, and policy monitoring.

However, B2B industrial equipment and machinery wholesale sectors that had high PPI but can easily pass on costs could directly translate to related companies’ performance. Worth studying (Related companies: Fastenal ($FAST), W.W. Grainger ($GWW)).

| Sector/Company Type | Pass-through Possibility | CPI Transmission Risk | Absorption Burden | Representative Companies |

|---|---|---|---|---|

| Industrial Equipment & Machinery Wholesale (B2B) | High | Low | Low | Fastenal, W.W. Grainger |

| General Retail (B2C) | Low | High | High | Walmart, Target, Costco |

| Food & Agriculture (B2C) | Low | High | High | Tyson Foods, Fresh Del Monte, Dole |

| Transportation & Logistics (B2C) | Low | High | High | FedEx, UPS, JB Hunt, Old Dominion |

| Energy (B2C) | Low | High | High | ExxonMobil, Chevron, Marathon Petroleum, Valero |

| Healthcare (Hospital Outpatient, etc.) (B2C) | Very Low | Low | Very High | HCA Healthcare, Tenet Healthcare |

| Consumer Goods Retail (Furniture, etc.) (B2C) | Very Low | Low | Very High | IKEA, Williams-Sonoma, Ashley Furniture |

| Energy Pipeline Transportation (B2B) | Very Low | Low | Very High | Kinder Morgan, Williams Companies |

| Financial Services (B2B/B2C Mixed) | Medium-Low | Low | Medium | Charles Schwab, BlackRock, Morgan Stanley, JPMorgan |

Looking at the overall trend graph, while there is an upward trend, it could be a one-time factor, so it doesn’t look seriously concerning. If we see consecutive readings above 1.0% in September, warnings might emerge.

Macro Check Summary

- Global economy maintains stable inflation with healthy CPI levels and recovering CCI trends

- Stocks remain more attractive than bonds, with clear fund inflows to emerging markets like Vietnam and Korea

- Gold and silver maintain high demand amid U.S. policy uncertainty, with silver showing steep gains from combined safe asset and industrial demand value

- PPI shows B2B industrial equipment/machinery sectors have high price pass-through potential and room for performance improvement, while B2C companies need monitoring for absorption capacity

- Considering interest rates, inflation, and demand flows, moderate optimism in economic expansion phase is valid

Sector Opportunity Analysis

Based on GICS 11 sectors + key investment opportunities:

- Technology: Growth confirmation more important than rate cuts (investment timing before earnings season in Oct-Nov, adjustment possible until then, especially hardware companies with overseas manufacturing face volatility exposure)

- Healthcare/Communications/Consumer Staples: Defensive characteristics favor safe asset preference period before Sep/Nov FOMC

- Industrials/Materials/Utilities/Energy: Continued benefits for U.S. factory-based companies under Made in USA policy

- Homebuilding/Utilities/REITs: Sensitive reactions expected to rate cut expectations and actual cuts

- Financials: Continued benefits from rate cut delays + additional opportunities from Made in USA investment expansion

Top priority sectors for August: Healthcare, Communications, Materials, Uranium, Energy, Lithium, Autonomous Vehicles

Key ETFs:

- XLV (IHI/IHF) – Healthcare

- XLC – Communications

- XLE (NLR/URA/NUKZ/IEZ) – Energy & Uranium

- XLI (ITA) – Industrials

- XLY (ITB/IDRV) – Consumer Discretionary

- XLRE (HOMZ) – Real Estate

- XLB (ILIT) – Materials

Focus areas: Economic defense + energy resources + autonomous driving (which hasn’t participated in tech rally but shows emerging visibility)

Investment Asset Opportunity Analysis

Bonds: While short-term bond positions may be attractive expecting September rate cuts, stocks (especially defensive sectors + Made in USA energy resources) offer relatively greater opportunities than bond capital gains amid expanding volatility.

Gold/Silver: Real assets that shine brightest in Trump-style economic volatility and U.S.-China conflict tensions. Not wasteful to hold in portfolios now.

Crypto: Now at a testing point. Can crypto, which has rallied alongside tech growth stocks, continue its upward trend when defensive stocks are preferred? Whether policy support for stablecoins can create solid flows backed by dollars and Treasuries is a key watching point.

Core Investment Theme: Made in USA

What would be the most important aspect of Trump’s policies in one phrase? Reducing trade deficits through tariffs? Establishing policy frameworks for cryptocurrencies? Making advanced IT/energy industries matters of national security? While there are various big frameworks, the core of “Make America Great Again” ultimately seems to converge on “Made in USA.”

Industries and companies that once focused only on efficient production according to Ricardo’s theory of comparative advantage now face changed future prospects based on whether manufacturing plants are located in the United States.

Therefore, Made in USA is becoming a definitive agenda that can be invested in regardless of macro environment. Here are key companies to watch:

Made in USA Key Companies by Sector

Semiconductors/IT & Electronics

- Intel ($INTC), Micron ($MU): Direct U.S. semiconductor fab operations, expanding government support

- TSMC ($TSM): Arizona large fab starts mass production 2025+

- Samsung Electronics (005930): Texas advanced fab production H2 2025

- Corning ($GLW), ON Semiconductor ($ON): Expanding materials/chip production plants in U.S.

- Nano Dimension ($NNDM): Massachusetts factory, expanding U.S. manufacturing ecosystem through M&A

- Ambarella ($AMBA): U.S. R&D/design, production cooperation with TSMC/Samsung/ON, high Tesla expansion potential

- Aehr Test Systems ($AEHR): SiC/EV semiconductor test equipment, U.S. factory, rapid export growth

Defense & Aerospace

- Boeing ($BA), Lockheed Martin ($LMT), Northrop Grumman ($NOC), General Dynamics ($GD): All major U.S. defense companies centered on U.S. mainland manufacturing

- Hanwha Ocean (042660): Philadelphia shipyard, strategic localization for U.S. Navy

Automotive & Steel

- GM ($GM), Ford ($F), Tesla ($TSLA), Hyundai (005380), Toyota ($TM), U.S. Steel ($X): All operating U.S. local assembly/steel plants directly

- Aptiv ($APTV): Automotive electronics/autonomous driving/EVs, large-scale U.S. and Mexico factory expansion

Healthcare & Pharmaceuticals

- Johnson & Johnson ($JNJ), Pfizer ($PFE): Multiple U.S.-concentrated production facilities

- AstraZeneca ($AZN), Novartis ($NVS): Full-scale U.S. bio production plants starting end-2025~26

Energy & Resources

- ExxonMobil ($XOM), Chevron ($CVX): Oil/gas production facilities distributed across U.S.

- Enphase ($ENPH), SunRun ($RUN): Solar/ESS, U.S. mainland manufacturing + localization (maximum IRA benefits)

- IES Holdings ($IESC): U.S. industrial/AI/electrical/data infrastructure solutions

- Cameco ($CCJ): World’s largest uranium/nuclear fuel supplier, expanding U.S. contracts and plant construction

Machinery & Heavy Industry

- Caterpillar ($CAT), John Deere ($DE): U.S. local production, infrastructure/agricultural machinery supply chain leaders

- Hyundai Steel (004020): Louisiana new steel plant, expanding EV/construction equipment steel supply

- Applied Industrial Technologies ($AIT): Automation/materials/components, expanding U.S. manufacturing network nationwide

Materials, Technology & Components

- Albemarle ($ALB): North Carolina lithium refining plant, maximizing IRA/U.S. government benefits

- LG Energy Solution (373220), SK Innovation (096770): New battery plants in U.S. South/Midwest

- MP Materials ($MP): Rare earth/EV materials direct production plants in U.S.

- DuPont ($DD), Dow ($DOW): Core chemicals/new materials, strengthening U.S.-focused local production/supply systems

I’ll provide detailed reviews of these companies when opportunities arise.